In-Depth Analysis Report on South Korea's Crypto Asset and Stablecoin Regulatory Policies

16/04/202612:10:59

Market Trends

Bifu Research | 2026

Abstract

The regulatory tone for cryptocurrencies in South Korea has undergone a historic shift over the past few years, officially moving from a nine-year period of "comprehensive prevention and blockade" to a new phase of "institutional entry and innovation support under a compliance framework." In early 2026, the South Korean government officially lifted the ban on corporate investment in cryptocurrencies, signaling the opening of the floodgates for compliant institutional capital.

Meanwhile, constrained by the legislative progress of core bills such as the Digital Asset Basic Act, South Korea's stablecoin market presents a distinct characteristic of a "policy vacuum coexisting with preemptive market actions." Traditional financial institutions are utilizing a "de facto sandbox" model via foreign exchange channels to deploy stablecoin payment networks on a massive scale.

Against this backdrop, the compliance pathways for stablecoins and Real-World Asset (RWA) tokenization are becoming increasingly clear. The extreme demand from South Korea's traditional financial sector for underlying blockchain infrastructure is catalyzing massive "white-label" infrastructure dividends and incremental market opportunities for tech providers equipped with cross-border settlement and compliance management capabilities.

I. Reshaping of South Korea's Regulatory Power Landscape

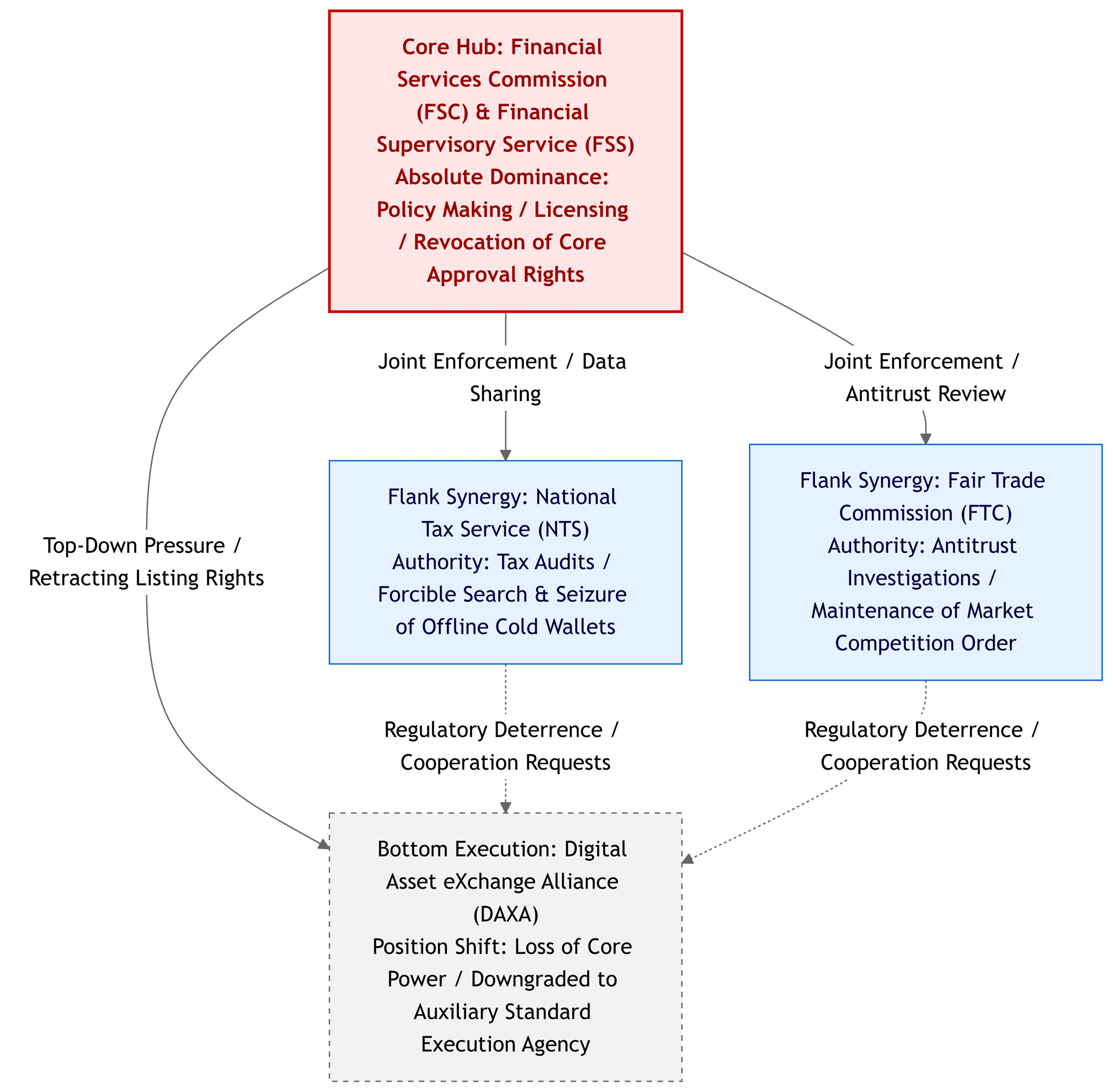

The current virtual asset regulatory system in South Korea is characterized by "one primary authority with multiple auxiliaries, and the centralization of power." The previous paradigm, where industry self-regulatory associations dictated market order, is collapsing as regulatory power rapidly concentrates within central financial regulatory bodies.

As South Korea's supreme financial decision-making body, the Financial Services Commission (FSC) and its subordinate Financial Supervisory Service (FSS) have established absolute dominance over virtual asset policy-making, VASP licensing, and daily compliance supervision. Recent policy actions indicate that the FSC is gradually retracting core privileges, such as "token listing approvals" previously held by major exchanges, through strict legislation to eliminate market opacity.

In terms of collaborative regulation, a multi-departmental joint enforcement framework has taken shape. Since 2025, the National Tax Service (NTS) has been empowered to conduct forcible searches and seizures of offline cold wallet assets belonging to suspected tax evaders, marking a comprehensive upgrade in tax enforcement. Concurrently, the Fair Trade Commission (FTC) has targeted oligopolistic exchanges (such as Upbit and Bithumb) that dominate the South Korean crypto market, launching antitrust investigations to maintain fair competition. Under this new landscape of stringent government oversight, the Digital Asset exchange Alliance (DAXA)—comprising South Korea's top five compliant exchanges—has been downgraded from an industry self-regulatory organization with the power of "joint delisting" to an auxiliary execution agency supporting the FSC's unified standards.

II. 2025-2026 Core Regulatory Policy Evolution: Institutional Entry and Compliance Trends

Entering 2026, South Korea's crypto regulation has hit an intensive period of policy implementation. While opening the doors to traditional institutions, regulators have simultaneously imposed unprecedented compliance pressures on Virtual Asset Service Providers (VASPs).

1. Epoch-making Institutional Entry Deregulation

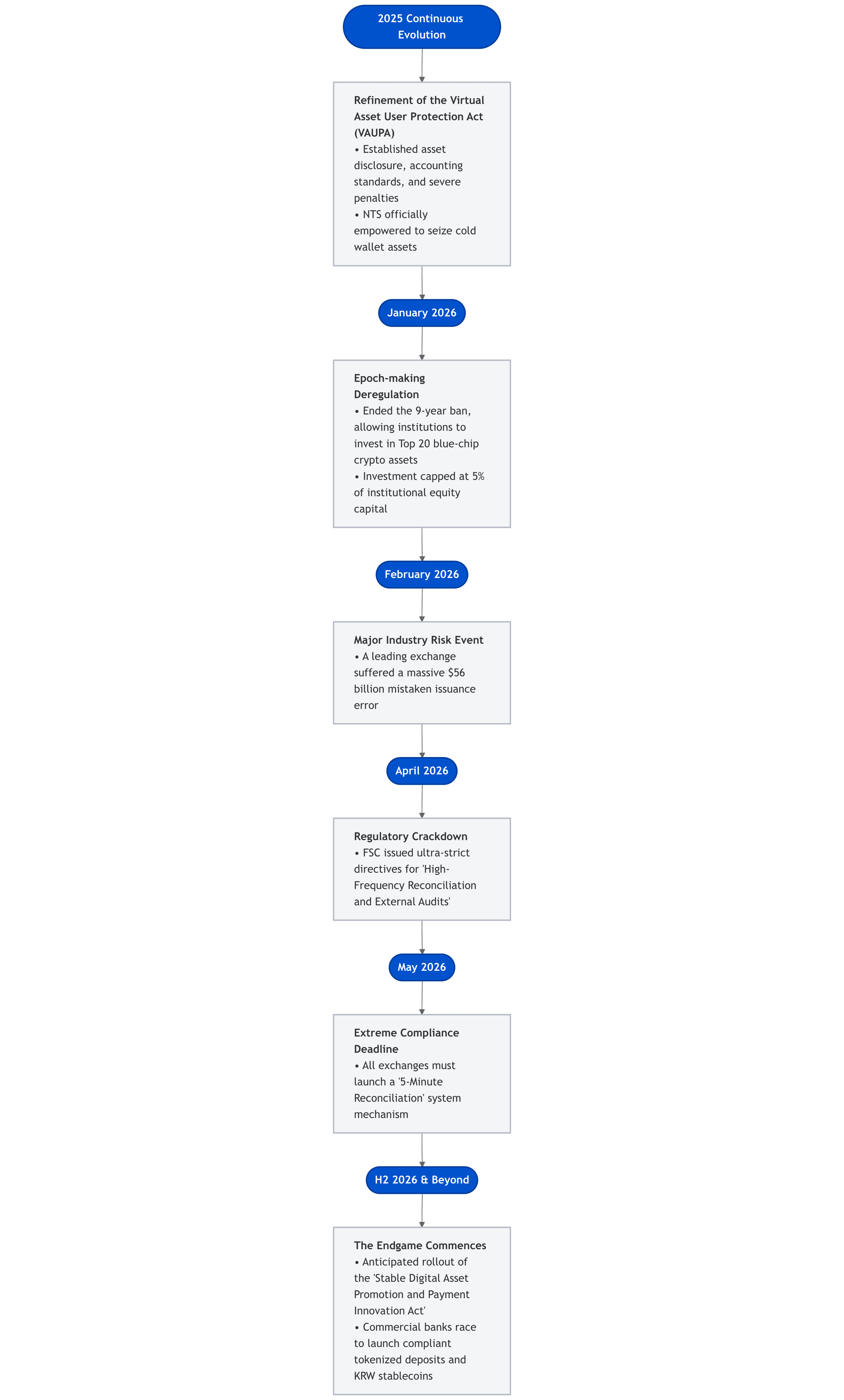

In January 2026, the FSC officially finalized guidelines to end the nine-year ban on corporate investment in cryptocurrencies, which had been in place since 2017. Under the new rules, approximately 3,500 listed companies and qualified professional investment institutions are permitted to invest up to 5% of their own capital (shareholders' equity) in cryptocurrencies. Preliminary estimates suggest that if merely 10% of the allowed 5% capital from listed companies translates into actual crypto allocations, it could bring billions to tens of billions of dollars in new liquidity to the market. To protect corporate balance sheets from the volatility of high-risk altcoins, regulators implemented an extremely strict "blue-chip whitelist" system, restricting institutional investments exclusively to the top 20 crypto assets by market capitalization (e.g., BTC, ETH) traded on South Korea's top five compliant exchanges.

2.The World's Strictest "5-Minute Reconciliation" Mechanism

While relaxing investment entry, regulators escalated internal control requirements for trading platforms to an extreme level. In February 2026, Bithumb, South Korea's second-largest exchange, accidentally issued approximately $56 billion worth of assets (around 620,000 BTC) to users due to an operational error. This severe risk event directly prompted the FSC to issue a stringent reconciliation directive in April of the same year: All South Korean crypto exchanges must launch a near real-time reconciliation system by the end of May 2026, accurately verifying customer ledgers against actual on-chain holdings at 5-minute intervals, and subjecting themselves to high-frequency monthly external audits. This extreme compliance requirement immediately burdened small and medium-sized exchanges with millions to tens of millions of dollars in IT restructuring costs, simultaneously spawning a massive incremental market for professional B2B on-chain data tracking and automated reconciliation tool providers.

3.Deepening of the Virtual Asset User Protection Act (VAUPA)

As the cornerstone of industry regulation, VAUPA continues to deepen. Following the early establishment of foundational frameworks such as cold wallet storage ratios and fiat segregation, the current regulatory focus has shifted to refining disclosure rules for asset issuance and circulation, establishing accounting standards for crypto assets under South Korean law, and supplementing these with severe criminal penalties for insider trading and market manipulation.

III. Stablecoin Policy Gaming and Financial Institutions' "Workaround Strategies"

Stablecoins currently represent a highly scrutinized "vacuum zone" in South Korean regulation, plagued by legislative lag. Amid intense friction between compliance redlines and market demand, a unique commercial spectacle has emerged locally.

In the recently implemented corporate investment deregulation guidelines, regulators drew a clear redline: to prevent chaotic capital outflows and protect the foreign exchange market, USD-pegged stablecoins like USDT and USDC are explicitly excluded from the whitelist of permitted investments for listed companies.

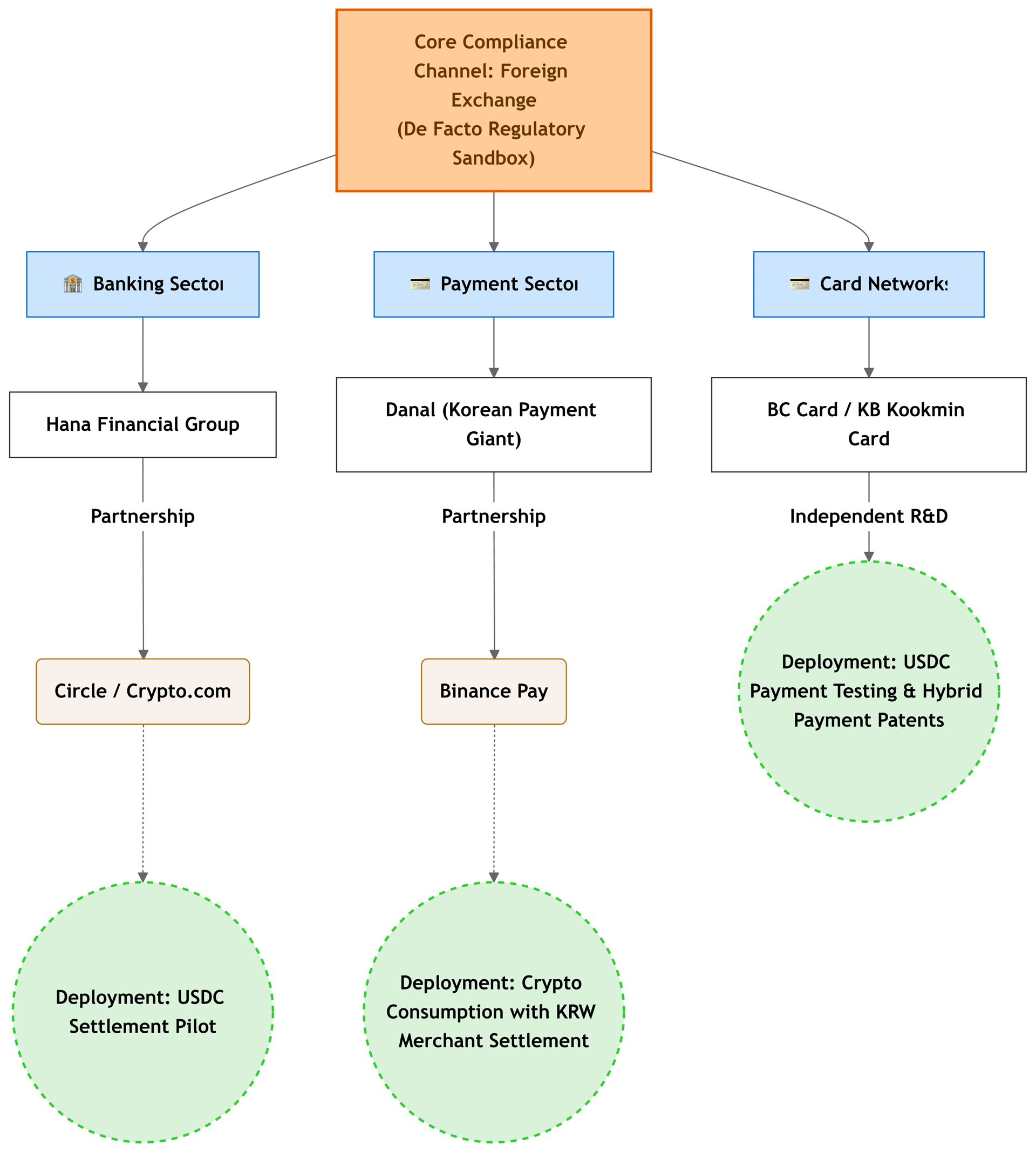

However, strict domestic regulations have not halted the preemptive moves of traditional financial giants. Due to delays in the Digital Asset Basic Act and stablecoin-specific legislation, domestic stablecoin businesses targeting South Korean citizens face immense barriers. Driven by profitability, South Korean financial institutions are conducting "de facto regulatory sandbox experiments" using "foreign exchange" as a compliance backdoor. Because crypto payment services provided to "foreign visitors" can be legally categorized under the Foreign Exchange Transactions Act, financial institutions can cleverly bypass the stringent domestic Virtual Asset Act.

Entering the first half of 2026, these preemptive institutional deployments have landed densely: Banking representatives such as Hana Financial Group, in partnership with Crypto.com, launched a USDC payment pilot for foreign visitors; payment giant Danal partnered with Binance Pay to introduce cross-border payments, achieving a closed loop of "crypto consumption by users, KRW settlement for merchants"; furthermore, traditional credit card organizations like BC Card and KB Kookmin Card are actively testing USDC payment technologies and applying for hybrid payment system patents. While ostensibly providing convenience for foreign tourists, these actions are essentially "strategic rehearsals" for traditional financial institutions to validate underlying payment technologies, streamline operational workflows, and secure partnerships with top-tier international players before domestic regulations fully open up.

Looking ahead, the emergence of the KRW Stablecoin forced by dedicated legislation will be the endgame of this chess match. The South Korean National Assembly is currently reviewing drafts proposing that stablecoin issuers must have at least 500 million KRW in capital and maintain 100% highly liquid reserves. Guided by the Bank of Korea, eight major commercial banks are accelerating the development of compliant "tokenized deposits" and KRW stablecoins, aiming to capture the pricing power of domestic currency payments in the future digital asset era.

IV. Growth Expectations for RWA and Tokenized Assets

While stablecoins face tight regulation and fierce competition, the tokenization of Real-World Assets (RWA) has received explicit endorsement at South Korea's national strategic level.

The South Korean government has officially designated Web3, GameFi, and RWA as core drivers of the digital economy. Guided by this strategy, the Korea Exchange (KRX) has been officially approved to operate a dedicated Security Token Offering (STO) market, providing an official trading venue for compliant on-chain assets. As funds from thousands of corporate institutions gradually enter the market, KRW-denominated tokenized government bonds and compliant yield-bearing tokens are poised for explosive growth. Furthermore, beyond standardized financial products, South Korea already possesses mature sandbox exploration experience in real estate yield tokenization (e.g., the early Kasa platform). The integration of these assets with the tokenized deposit-based financial derivatives currently being developed by traditional banks is expected to rapidly become the next core growth engine of South Korea's capital market.

V. Market Outlook and Investment Insights

Observing the policy trajectory from 2025 to 2026, South Korea is reshaping its cryptocurrency market ecosystem through a strategy of "strictly controlling systemic risk while precisely greenlighting institutional entry." The core market trends and opportunities for the future likely include:

1. Focus on Compliant Infrastructure and Payment Sector Opportunities

South Korean traditional financial institutions are highly motivated to enter the stablecoin and crypto settlement networks but heavily rely on mature external technical infrastructure. For general investors, ecosystem projects equipped with cross-border settlement capabilities, underlying public chain adaptability, and compliant wallet technologies will undergo a major value reassessment during this transition period. Tokenization protocols capable of providing "infrastructure bridging" for large traditional institutions warrant significant attention.

2. Institutional Entry Reshapes Market Structure, Favoring Value Coins Long-Term

With approximately 3,500 listed companies and professional institutions granted entry (utilizing up to 5% of their equity), the era of retail dominance in the South Korean market (characterized by the "Kimchi Premium" and altcoin speculation) is receding. Constrained by the compliance whitelist, institutional funds will inevitably concentrate on the Top 20 "blue-chip" crypto assets (e.g., BTC, ETH). Simultaneously, projects in the institutional-grade asset management, secure custody, and AML/KYT compliance sectors are expected to become the next hotspots chased by institutional capital.

3. Preemptively Capture the KRW RWA and Tokenized Asset Ecosystem Dividend

The stablecoin cross-border payment pilots are merely the beginning; KRW-denominated RWAs based on compliance frameworks (tokenized deposits, tokenized government bonds, etc.) represent the ultimate endgame in the game between regulators and traditional finance. Bifu users should closely monitor the liquidity spillover effects of South Korea's official STO market, as well as cross-chain and RWA underlying protocols that establish deep partnerships with local South Korean financial networks, as these will be key targets for capturing the next cycle's dividends.

4. [Risk Warning] Beware of Short-Term Volatility During the "Policy Window"

The current stablecoin boom based on the "foreign exchange channel" bears the attributes of a "de facto sandbox." Once the specific rules of the Digital Asset Basic Act are fully implemented, it is highly likely that the FSC will tighten existing foreign exchange shortcuts and mandate all participants to migrate to locally licensed KRW stablecoin networks. Users are advised to closely monitor the actual implementation dynamics of South Korean regulatory policies when investing in stablecoin and payment-concept sectors, ensuring flexible asset allocation and risk hedging.

VI. References

- Financial Services Commission (FSC) . (2026). Guidelines and Notice on Easing Limits for Corporate Investment in Virtual Assets. Retrieved from: https://www.fsc.go.kr

- Financial Supervisory Service (FSS) . (2026). Directive on Strengthening High-Frequency Reconciliation and External Audits for Virtual Asset Trading Platforms. Retrieved from: https://www.fss.or.kr

- National Policy Committee of the National Assembly . (2025). Digital Asset Basic Act (Draft) and Regulatory Rules for Stablecoin Issuance. Retrieved from: https://www.assembly.go.kr

- The Korea Times . (2026). Korean financial giants race to build stablecoin infrastructure amid regulatory lag. Retrieved from: https://www.koreatimes.co.kr

Disclaimer

This report is compiled by Bifu Research Institute and is for informational reference only. It does not constitute any investment advice, legal opinion, or endorsement of specific assets. The digital asset market has high volatility and risk; past performance does not represent future returns. Users are advised to fully assess risks and consult professional advisors before investing.

The policy interpretations covered in this report are based on the regulatory environment at the time of publication. Because local laws and regulations may update and adjust over time, specific compliance requirements should always be subject to the latest documents released by official regulatory agencies. Bifu assumes no legal responsibility for any decisions made based on this report.