Tokenized Treasury Bills: The Rise of On-Chain Risk-Free Rates and the Restructuring of Asset Allocation

29/12/202502:20:14

As the global macro-financial environment evolves, the digital asset market is undergoing a profound fundamental restructuring from "endogenous speculation" to "exogenous value." When the US Dollar risk-free rate becomes the anchor for global asset pricing, holding non-interest-bearing stablecoins implies a significant opportunity cost.

Tokenized Treasury Bills—the fastest-growing and most standardized category within the Real World Asset (RWA) sector—are becoming the critical transmission mechanism connecting Traditional Finance (TradFi) with On-Chain Finance. Based on the latest market data from 2025, this report delves into the competitive landscape and operational logic of tokenized treasuries, analyzing the irreplaceable role of Centralized Exchanges (CEX) in solving liquidity friction and entry barriers.

Paradigm Shift: From "Zero-Yield Assets" to "Interest-Bearing Assets"

In the early stages of digital assets, market yields often stemmed from high-risk liquidity mining, lending protocol mismatches, or inflationary token rewards. This endogenous yield model was highly dependent on market sentiment and exhibited clear cyclicality. The core significance of tokenized treasuries lies in introducing Exogenous Yield on-chain at scale, providing the crypto market with a genuine "risk-free rate" benchmark synchronized with traditional finance.

Capital Voting

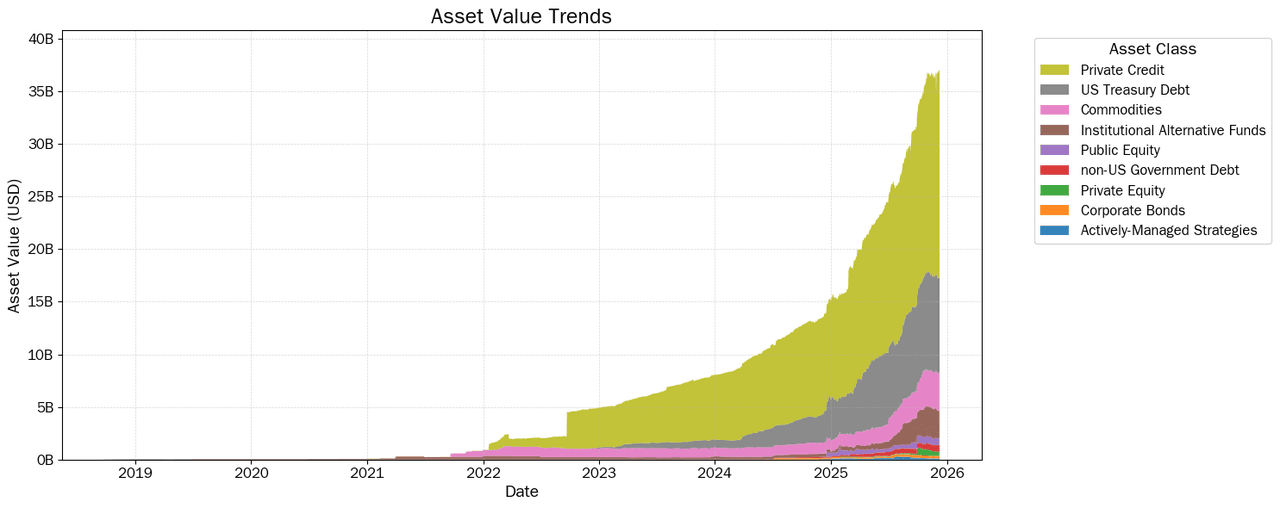

According to the latest market research and statistics from RWA.XYZ, as of December 11, 2025, the total global RWA asset scale (excluding stablecoins) has surpassed $37.11 billion. Among them, Tokenized Treasury Bills are the fastest-growing and most standardized segment, although their absolute scale currently trails private credit.

This growth trend indicates that capital is accelerating from simple stablecoins into on-chain instruments capable of capturing US Treasury yields. Institutional investors and high-net-worth individuals are no longer satisfied with mere capital transmission; they are integrating on-chain asset allocation into their mainstream horizons, seeking the maximization of capital efficiency.

Concept Distinction: Platform Marketing vs. Asset Rights

When discussing interest-bearing assets, there is often conceptual confusion in the market. We must clarify the essential difference between "Platform Yield" and "Native Yield" based on asset attributes.

- Platform Yield: Often a Marketing Yield strategy by exchanges or wealth management platforms. The platform invests its fiat reserves in treasuries and returns a portion of the earnings to users as subsidies. In this model, users hold a claim against the platform, not direct rights to the underlying asset, and yields are subject to the platform's commercial decisions.

- Native Yield: This is the core value of RWA. Taking BlackRock’s BUIDL or Ondo’s USDY as examples, the token itself represents rights to the underlying trust or fund shares. Yields are typically written directly into the smart contract via Rebase (automatic share increase) or Accumulating (Net Asset Value growth) mechanisms. This model promotes a deep binding of yield rights with the asset itself, realizing the true return of asset ownership.

Market Landscape: The Matthew Effect and Model Stratification

Market data from 2025 shows that the tokenized treasury market has exhibited a significant concentration at the top (The Matthew Effect), while also deriving diversified operational models to adapt to different investor needs.

Strong Entry of Traditional Financial Institutions

Institutional-grade products are currently the mainstream force in the market. They are typically issued directly by traditional financial giants and possess strong compliance backing.

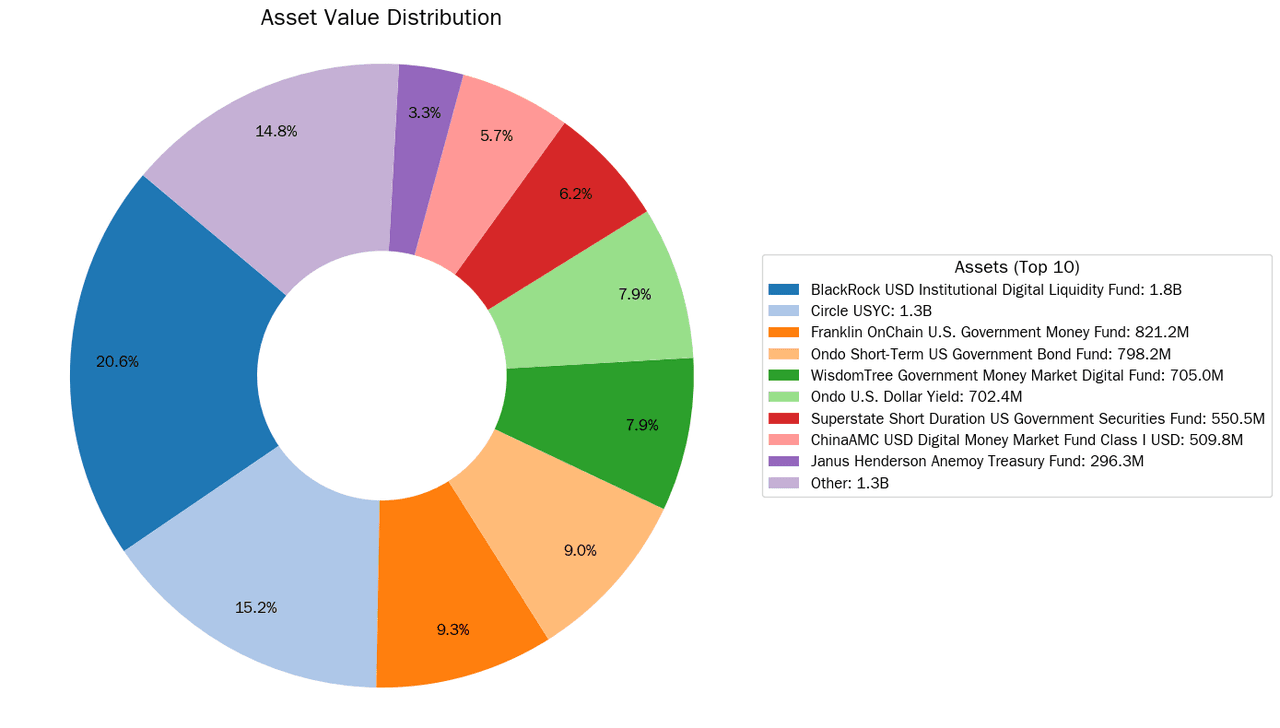

- BlackRock BUIDL: Currently occupying a dominant position with approximately 20% market share. By partnering with top institutions like Circle, this product has achieved superior liquidity support. It is primarily strictly for institutional investors, featuring high minimum investment thresholds and whitelist mechanisms.

- Franklin Templeton: Its FOBXX fund has extensively deployed on public chains like Stellar and Polygon, maintaining a low management fee of approximately 0.15%. This demonstrates the advantage of traditional asset management giants in technical application and cost control.

Flexible and Innovative Web3 Institutions

Beyond traditional giants, Web3 innovative institutions represented by Ondo Finance and Matrixdock tokenize ETFs through SPV (Special Purpose Vehicle) structures. These are more compatible with the crypto ecosystem, supporting collateralization in lending protocols, thus solving the composability issue of RWA assets.

Analysis of Asset Issuance Paths

Regarding asset structure, the market primarily follows two paths: Asset-Backed and Synthetic.

- Asset-Backed: Every token is backed by real assets held in custody by licensed banks, featuring clear bankruptcy remoteness mechanisms. The flagship products of BlackRock, Franklin Templeton, and Ondo all fall into this category.

- Synthetic: Mostly synthetic asset contracts tracking prices, involving no direct ownership of the underlying assets.

From the perspective of long-term robust development, tokens with a genuine bankruptcy-remote architecture are better equipped to withstand extreme market risks and are bound to become the mainstream direction for asset selection in the industry.

The Bridge Value of Exchanges: Liquidity and Access Layer

Although asset issuance occurs on-chain, industry reality shows that the vast majority of potential users remain on centralized platforms. To move RWA from an "Institutional Game" to "Mass Adoption," Centralized Exchanges (CEX) play a crucial role. This is determined not only by trading habits but also by the characteristics of RWA assets themselves.

Buffering "T+N" Liquidity Friction

Subscription and redemption of compliant treasury funds usually follow traditional banking timelines, requiring T+1 or even T+2 business days. Furthermore, they are constrained by banking hours, with no settlement on weekends. This creates a massive mismatch with the crypto market's habit of 24/7, instant settlement.

Exchanges possess a unique advantage in this link. By building multi-tiered liquidity buffer pools, platforms can internally digest redemption requests, providing users with a fast redemption experience superior to on-chain processes. This "savings-account-like" liquidity service can significantly reduce the time cost for users participating in RWA and is a key link connecting Web2 efficiency with Web3 assets.

Breaking the Wall between "Wholesale and Retail"

As mentioned, top RWA projects often set extremely high capital thresholds (e.g., $5 million minimum) and cumbersome KYC processes, greatly restricting participation paths for retail users.

Exchanges can function as "Aggregators." Through compliant asset management architectures or fund share splitting, they can transform large-scale institutional assets into low-threshold retail products. Users can obtain institutional-grade treasury yield exposure without mastering complex on-chain operations. This capability of "Wholesale to Retail" is the necessary path for the scaled expansion of RWA.

Potential Release of Capital Efficiency

From a longer-term perspective, RWA promises to reshape capital efficiency in trading scenarios. Currently, traders pledge large amounts of non-interest-bearing USDT in contract trading. The industry is actively exploring the possibility of incorporating high-quality tokenized treasuries into a Unified Margin System. In an ideal state, a trader's idle margin could automatically earn treasury interest, while seamlessly serving as collateral when opening positions. If this "Interest-Bearing Margin" model can be implemented, it will vastly improve the market's capital utilization rate.

Risk Assessment and Industry Outlook

While embracing the RWA wave, a multi-dimensional risk assessment framework must be established. Integrating deep industry research and market practice, participants should focus on the following dimensions:

Legal Finality and Bankruptcy Remoteness

Whether on-chain token holders legally possess disposal rights over off-chain assets is the core proposition of RWA. When evaluating assets, key considerations include whether the issuer operates in jurisdictions with mature legal frameworks (such as Singapore, Switzerland, UAE) and whether there is a clear Bankruptcy Remoteness mechanism. This ensures that in extreme scenarios, SPV assets are prioritized for repayment to token holders rather than the project's creditors.

Technology and Data Source Risks

Beyond routine smart contract audits, RWA assets face risks regarding off-chain data coming on-chain. The stability of Oracle Price Feeds is crucial; precautions must be taken against token price de-pegging caused by off-chain data anomalies or price lags due to stock market closures.

Future Trends: Convergence and Interoperability

Looking ahead, RWA development will present two trends:

- Deep Integration of On-Chain and Off-Chain: Traditional financial institutions will no longer serve merely as custodians but will participate directly as nodes in on-chain issuance. The boundary between deposit tokens and treasury tokens will become increasingly blurred.

- Cross-Chain Interoperability: With the maturation of cross-chain technologies like CCIP, tokenized treasuries will no longer be confined to a single blockchain but will flow freely across multi-chain ecosystems. For trading platforms, supporting multi-chain deposits/withdrawals and providing cross-chain liquidity will become a core competency.

Conclusion

Tokenized Treasury Bills are not a short-term hype in the crypto world, but a significant evolution in the long river of financial history. They transform the "risk-free rate" from a patent of traditional finance into a programmable cornerstone of the digital economy.

For Bifu, we closely monitor this historical process and are committed to exploring—through technological and product innovation—how to act as a Selector of high-quality assets and a Provider of liquidity. Whether through compliant underlying asset access or flexible liquidity services, we will continue to build a bridge for users to a secure, interest-bearing, and efficient new world of digital finance.

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.