DAT to RWA: A Comprehensive Model Analysis

19/11/202507:41:08

From Strategic Reserve to Financial Infrastructure: Comprehensive Analysis of the DAT Model and RWA Endgame Deduction.

Introduction

On November 13, 2025, the market once again turned its attention to MicroStrategy—the listed company known for its Bitcoin holdings saw its market capitalization briefly fall below the value of its Bitcoin holdings. This phenomenon quickly triggered concern, but the reason behind it is not complex: this calculation did not take into account the convertible notes, preferred stock, and other instruments issued by the company, which enjoy priority over common stock in liquidation. If measured by a more comprehensive Enterprise Value, the company's total value remains higher than its Bitcoin holdings.

In fact, over the past few years, MSTR stock has traded at a significant premium almost consistently, sometimes reaching 1.5 to 2 times the value of the underlying Bitcoin assets.

This raises a more worthy question: Why are investors willing to pay a significant premium to hold MSTR, rather than directly buying a simpler, more transparent, and lower-fee BTC ETF?

The reason is that MicroStrategy's model is not equivalent to a "Bitcoin holding company." The company raises funds by issuing convertible notes, preferred stock, etc., and then reinvests the capital into Bitcoin, thereby forming a leveraged Bitcoin exposure carried by the corporate balance sheet. What investors are buying is not a simple Bitcoin reserve, but a "leveraged" Bitcoin risk exposure constructed by the enterprise using credit expansion.

As this model is adopted by more companies, a new classification concept is gradually emerging in the market: these companies that use the "Issue Debt—Buy Coins—Refinance" mechanism to amplify crypto asset exposure are being called the next darlings of the crypto market—DAT Companies (Digital Asset Treasury). Next, this article will use the touch of in-depth news analysis to systematically disassemble the definition, structure, risks, and investment logic of DAT companies, and analyze why they have become the focus of attention for both traditional capital and crypto capital in the current cycle.

What is a DAT Company?

DAT (Digital Asset Treasury) refers to a company that incorporates digital assets (such as BTC, ETH) into its corporate balance sheet as strategic reserve assets and holds and manages them in an institutionalized, cross-cycle manner. It is a financial strategy, not short-term speculation; it is a treasury system written into corporate governance processes, not impromptu investment by management.

The essence of DAT is that enterprises treat digital assets as long-term, verifiable reserve assets with macroeconomic functions, using the corporate balance sheet to carry this exposure. For example, MicroStrategy's buying actions throughout the bull and bear markets over the past three years, and Metaplanet positioning Bitcoin as a "long-term corporate reserve asset" against Yen depreciation, all demonstrate the same orientation: digital assets assume the role of a "long-term stabilizer" in the enterprise's balance sheet, rather than a side investment that can be discarded at any time.

Based on this logic, the uniqueness of DAT is further reflected in the changes in the balance sheet structure. Traditional enterprises usually view digital assets as an optional investment target, but the characteristics of DAT are exactly the opposite: they embed digital assets into the core asset structure of the enterprise, making them part of capital allocation and long-term strategic planning. Tesla's initial purchase of Bitcoin was driven by the hope of transforming part of its cash reserves from "static dollar assets" into strategic assets with long-term return potential; Block incorporated Bitcoin into its long-term holding asset system, making it part of the company's payment ecosystem and brand philosophy. This shows that for DAT, holding digital assets is not to capture short-term gains, but to make the balance sheet more aligned with the needs of the future macroeconomic environment and long-term corporate strategy.

The on-chain attributes of digital assets give the DAT treasury structure a transparency that traditional assets find hard to achieve. Enterprises can expose their holdings in real-time on the chain by disclosing wallet addresses, allowing investors to monitor asset dynamics directly without waiting for quarterly financial reports. MicroStrategy disclosing corporate wallets is a typical example, and the Proof-of-Reserve mechanism increasingly adopted by mining companies and custodians also shows that the market is accepting on-chain verifiability as a new audit path. Transparent, independent of complex valuation models, and verifiable in real-time—this allows DAT's treasury disclosure level to significantly surpass traditional assets, significantly reducing investors' trust costs in the company's asset status.

More importantly, the formation of DAT is not the personal preference of management, but an institutional arrangement written into the corporate governance structure. Whether it is Tesla or Block, they have publicly disclosed digital asset holding policies, risk management frameworks, and accounting treatment standards in their financial reports; MicroStrategy has formulated a complete "Bitcoin Treasury Policy", systematically standardizing the acquisition process, custody methods, and governance mechanisms. This means that the establishment of DAT has continuity, auditability, and traceability; it is not a short-term experiment, but a long-term financial strategy approved by the board of directors and guaranteed by internal systems.

Overall, the rise of DAT reflects a paradigm shift in corporate treasury management: digital assets are no longer a question of "whether to hold" for enterprises, but are gradually evolving into a question of "how to incorporate into the balance sheet management system." Through strategic holdings, balance sheet restructuring, on-chain transparency, and institutionalized governance, enterprises establish digital assets as a long-term corporate reserve asset. This makes DAT different from traditional coin-holding companies and crypto business companies, but a new type of enterprise characterized by treasury structure, which is becoming a key window for the capital market to observe changes in corporate asset structure and evaluate long-term competitiveness.

The Rise of the DAT Model

DAT's evolution from early "individual company behavior" to a replicable corporate balance sheet strategy is not accidental, but driven by three forces: macro cycle, accounting system, and institutional allocation. Together, they make incorporating BTC/ETH into the treasury no longer a "risky behavior" for enterprises, but an asset management decision with a clear incentive structure.

1.Macro Environment: Global Liquidity Expansion and Fiat Purchasing Power Erosion

The speed of central bank balance sheet expansion after the pandemic has made it increasingly difficult for companies to ignore the opportunity cost of holding cash. The rapid growth of M2 and the long-term maintenance of low interest rates by major economies have weakened the "store of value function" of fiat currency in the balance sheet. In this environment, management is more inclined to look for alternative reserve assets that can circulate across regions, resist inflation, and have high liquidity.

In this context, it is not difficult to understand why BTC/ETH have become viable candidates. Compared with the cross-border friction of gold and the actual negative interest rate environment of government bonds, the "global pricing + no sovereign risk" attributes of digital assets fit the needs of multinational enterprises better. The macro rationality of DAT thus has an institutional starting point.

2.Accounting System Reform: FASB's "Unlocking" Incorporates Digital Assets into Mainstream Financial Logic

The key node for DAT to enter the balance sheets of more enterprises appeared around the FASB accounting standard reform in 2024.

Before the reform, digital assets were classified as intangible assets, and only impairment could be recognized, not appreciation. This not only biased the corporate income statement severely negatively but also made it difficult for CFOs to explain the financial significance of holding coins at board meetings.

After the reform, the introduction of fair value measurement implies:

- Coin price increases can be reflected in the income statement in real-time.

- Corporate book value is no longer passively suppressed.

- The risks and returns of holding digital assets are no longer distorted by the accounting system.

This is actually equivalent to a "institutional shot in the arm." DAT is no longer a political risk for CFOs but has been transformed into a normal asset allocation behavior that can be quantified, explained, and audited. This is also the main reason for the jump in BTC holdings by US listed companies after 2024.

3.Institutional Demand: ETFs Provide Mature Compliance Infrastructure for Enterprises

The large-scale release of Bitcoin spot ETFs has further promoted the diffusion of DAT. The ETF's custody system, audit process, insurance mechanism, and secondary market liquidity provide enterprises with a "standardized way of holding coins" that can be adopted directly.

This change brings two layers of impact:

- Management Risk Perception Change: Digital assets have changed from "high-volatility experiments" to "institutional-grade assets," similar to how Gold ETFs promoted gold allocation at the corporate level.

- Lower Execution Difficulty: Enterprises do not need to study cold wallets, custody security, or on-chain operations; they only need to purchase ETFs through brokers to complete the DAT treasury allocation.

Therefore, when the investment committee within an enterprise discusses balance sheet optimization, digital assets possess comparability and executability for the first time. It is no longer "something only crypto companies do," but has become an optional module for large corporate treasury management.

Driven by macro liquidity, accounting systems, and institutional adoption, the formation of DAT is not just a change in corporate asset allocation preferences, but is gradually developing a capital structure mechanism capable of self-reinforcement. As the price of Bitcoin rises, the market capitalization of enterprises usually rises synchronously, and the market will reprice these companies according to the logic of "quasi-BTC ETFs." The rise in market capitalization allows enterprises to enter the financing market at a lower cost of capital. Whether through convertible notes, preferred stock, or additional issuance at a lower discount, the financing window will be wider and deeper than that of ordinary enterprises.

After the financing cost drops, the enterprise has the conditions to continue increasing its BTC holdings, and this increase itself further increases the weight of digital assets in the corporate balance sheet, making its stock price increasingly sensitive to BTC. Consequently, once the Bitcoin price continues to rise, the company's market capitalization will react with higher elasticity, and market sentiment and valuation premiums will amplify accordingly, eventually giving the enterprise the ability to finance at a lower cost again.

This cycle has been fully verified in MicroStrategy and Metaplanet: stock price increases bring improved financing capabilities, financing brings greater coin-based exposure, and greater exposure strengthens the stock price's adherence to BTC. When enterprises institutionalize coin purchasing behavior and write it into treasury policies, this cycle gradually evolves into a flywheel effect, making the DAT model no longer just a simple choice of "buying coins," but a capital structure flywheel composed of balance sheet operations, capital market feedback, and scarce asset appreciation.

The existence of this flywheel explains why the DAT model has exploded in this cycle, and also explains why more and more enterprises are beginning to view digital assets as strategic reserves rather than short-term investments. The core of DAT lies not in betting on prices, but in utilizing the structural interaction between the capital market and the balance sheet to turn digital assets into long-term tools that can amplify corporate value.

Current State of the DAT Market

1.Market Scale Expansion: DAT Has Become an Important Strategic Asset Class

Over the past two years, the adoption rate of the DAT model at the corporate level has significantly accelerated. According to The Block reports, some DAT companies have added over 1.013 million Bitcoins (approx. 1,013,000 BTC) since 2024, corresponding to a market value of $113.9 billion. This large-scale expansion reflects that enterprises are shifting from fringe experiments to systematic allocation of crypto assets, especially Bitcoin.

This trend not only increases the capital volume of DAT itself but also strengthens its dual attribute of "Enterprise + Digital Assets" in valuation logic: more and more companies are treating digital assets like Bitcoin as a core component of their balance sheet rather than purely speculative exposure.

2.Currency Distribution: BTC Drives Growth, Diversification is Underway

In the currency composition of total DAT assets, Bitcoin (BTC) remains absolutely dominant. As a first-tier asset, it is not only included in the treasury strategies of more and more companies, but its holding scale and market value proportion support the accelerated growth of the overall DAT market.

At the same time, Ethereum (ETH) and Solana (SOL) are gradually becoming second-tier assets. Although their total scale in DAT is far less than BTC, long-term reserves at the corporate level are accumulating, indicating that the DAT model is stepping out of the single-asset stage of Bitcoin and expanding to a broader blockchain ecosystem.

Some other chain assets in the third tier (such as some Layer-1 tokens) also appear in corporate treasuries, but their current proportion is still small, mainly playing a strategic supplementary role rather than a main driver.

| Total USD Value | Total Institution | % of Circulating Supply |

BTC | $83.967b | 36 | 4.70% |

ETH | $15.76b | 16 | 4.39% |

SOL | $2.262b | 11 | 2.99% |

3.DAT Participating Company Type Structure Analysis

- Reserve Type (Pure Treasury): These companies mainly use digital assets as strategic reserve assets, and their financial exposure is centered on holding coins. Typical representatives include MicroStrategy (MSTR), Semler Scientific (SMLR), and Metaplanet (Japan). Their DAT strategies are very "treasury first," and their faith in Bitcoin is the firmest.

- Business-Driven Type: Although the core business of these companies is not crypto mining, they incorporate digital assets into their treasury for reasons of business synergy, strategic reserve, or payment ecosystem. Representative companies include Tesla (converting part of cash to BTC as reserve), Block (SQ/Block) (payment ecosystem and BTC reserve), Coinbase (COIN) (dual role of exchange + reserve). This type of DAT model does not center solely on BTC but uses coins as a tool for asset structure optimization.

- Mining Companies (Production + Reserve): As producers of digital assets, mining companies have a natural advantage in the DAT model. Companies like Marathon Digital (MARA) and Riot Platforms (RIOT) are responsible for both mining and long-term reserves. This allows them to sell mined coins and hold coins long-term like DAT companies; the two strategies overlap but differ.

- Other/Hybrid Type: There are also some companies that distribute their reserve assets in on-chain assets other than BTC and ETH (such as Solana, BNB, etc.), or operate through complex capital structures. Although not yet mainstream, the market has begun to pay attention to whether companies are attempting to incorporate Tokenized Treasury Bills (RWA) into their treasuries to replace low-yield stablecoins.

Backtesting Trends and Net Asset Premium Analysis of the DAT Model

In the previous section, we discussed the definition, structure, market background, and type distribution of DAT. Now we will focus on its specific trend performance in the capital market, analyzing MSTR as a typical case.

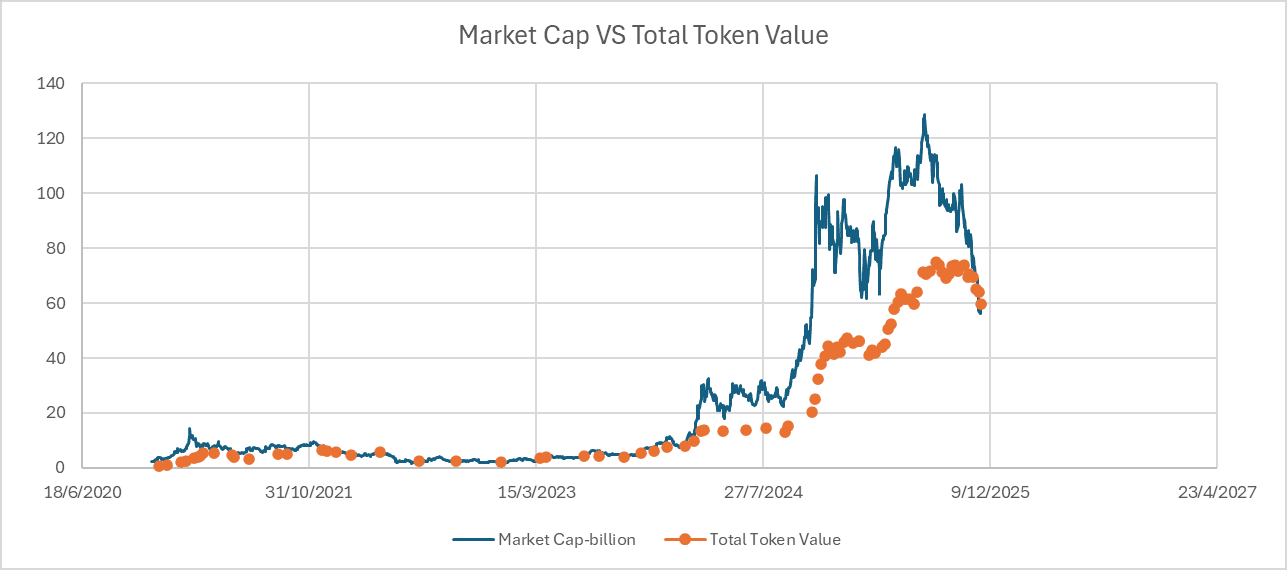

Structurally, the stock price of DAT companies is not only affected by their main business but is also directly bound to the floating value of the digital asset exposure in their balance sheet. This brings a key valuation indicator to the surface: the ratio of company market capitalization to the value of its digital asset reserves (mNAV). If this ratio is higher than 1x, it indicates that the market pays a premium for the company higher than the reserve assets themselves; if it is lower than 1x, the market gives a discount treatment.

Taking MSTR as an example, based on historical data, the following characteristics can be observed:

- Premium/Discount Volatility: During cycles of significant Bitcoin price increases, MSTR stock price usually shows super-proportional growth, causing the "Market Cap / Holdings Value" ratio to rise, indicating that the market pays a premium for its strategic reserves. When Bitcoin prices consolidate or fall, this ratio falls back below 1, indicating that the market gives a discount, and investors revalue the digital asset exposure of the corporate balance sheet.

- Market Reaction Lag and Sensitivity: The reaction of stock price to holding value has a certain lag, and the ratio changes more obviously during periods of high volatility. Backtesting shows that whenever MSTR announces news of new coin purchases or financing, the ratio will adjust quickly in the short term, reflecting the market's sensitivity to the corporate balance sheet strategy.

- Premium/Discount Interval Analysis: Historical data shows that the center of MSTR's "Market Cap / Holdings Value" ratio fluctuates in the 0.7–2x range over the long term, but briefly broke through 3x or even 5x during periods of high bull market sentiment (such as early 2021 and mid-2024). The high points correspond to the Bitcoin bull market, and the low points correspond to the bear market or market adjustment stages. This interval provides a quantitative basis for observing the relationship between the market capitalization of DAT companies and their strategic reserves.

Future Outlook: From Strategic Reserve to Active On-Chain Treasury

This report has systematically analyzed the definition, driving forces, and market status of the DAT model, demonstrating its rise as an institutionalized treasury strategy. As this model is adopted by more enterprises, its evolutionary path, secondary effects, and interaction with the broader on-chain economy (such as RWA) will become the focus of observation in the next stage. Based on current trends, we predict that the future of the DAT model will present four key trends:

1.Asset Expansion: From BTC Core to "BTC+RWA" Hybrid Treasury

Current DAT treasuries utilize BTC as the core, serving as "digital gold" for enterprises, primarily undertaking anti-inflation and long-term reserve functions. However, corporate treasuries also have "liquidity management" and "short-term cash yield" needs. As RWAs, especially tokenized short-term treasury bills, gradually mature in compliance and liquidity, the DAT balance sheet will move from "Digital Asset Reserve" to "On-Chain Asset Reserve." Future hybrid DAT treasuries may form a two-layer structure:

- Macro Hedge Layer: Utilizing BTC as the core value reserve to cope with macro uncertainty.

- Liquidity/Yield Layer: Allocating operating cash to tokenized RWAs to obtain stable returns while ensuring high liquidity.

This will expand the role of the DAT treasury from a single store of value to a comprehensive on-chain balance sheet combining macro hedging, yield management, and efficient settlement.

2.Cyclical Risk: From "Leverage Flywheel" to "Deleveraging Spiral"

The DAT capital structure flywheel can enhance corporate market value performance in a bull market by financing and adding leverage to buy BTC. But its risk is symmetrical: in a bear market or liquidity crisis, this flywheel may reverse into a "Death Spiral." Its mechanism includes:

- BTC falls → DAT company market cap and mNAV shrink significantly.

- Market cap falls → Triggers debt covenants or refinancing difficulties.

- Forced selling of BTC → Further depresses BTC price → Further weakens market cap.

With the spread of high-leverage DAT strategies, this collective deleveraging behavior may become a new type of systemic risk in the crypto market.

3.Strategy Evolution: From "Passive Holding" to "Active Treasury Management"

"Reserve-type" DAT companies represented by MicroStrategy currently mostly adopt passive holding strategies. But as the asset scope expands to second-tier assets like ETH and SOL, their on-chain native yield (such as Staking) value will become increasingly important. Future DAT strategies may evolve towards "Active Treasury Management," including:

- Using ETH/SOL to participate in compliant on-chain staking to generate stable yields.

- Using assets as collateral to participate in on-chain financial protocols to improve capital efficiency under controllable risks.

This will significantly raise the requirements for DAT companies regarding risk control capabilities, on-chain operational capabilities, and transparent auditing.

4.Emergence of New Business Forms: The Rise of "DAT-as-a-Service" (DaaS)

Although ETFs and accounting system reforms have lowered the threshold for enterprises to allocate digital assets, once enterprises upgrade from "holding ETFs" to "allocating native assets + RWA + on-chain yield generation," the complexity of compliance, operations, and accounting treatment will rise sharply. Most traditional enterprises do not have the ability to manage on-chain treasuries independently. Therefore, a brand-new B2B track—DAT-as-a-Service (DaaS)—is expected to develop rapidly, providing enterprises with:

- Asset allocation and RWA access.

- Compliant multi-sig and custody systems.

- Automated on-chain yield strategies (e.g., Staking).

- Automated financial statements compliant with standards like FASB.

The maturity of DaaS will become the key infrastructure for the DAT model to move from "pioneer enterprises" to "mainstream enterprises."

5.Endgame Deduction: From "Treasury Strategy" to "Financial Infrastructure"

The previous four outlooks are based on the premise of the "dual-track parallel" of the current financial system and blockchain. However, when we push our perspective to the further future—a world where stablecoins become the main medium for payment, settlement, and investment—the meaning of DAT will undergo a fundamental transformation.

(1) DAT will become the infrastructure of corporate operations, not an "option"

When corporate accounts receivable, accounts payable, supply chain finance, and even employee salaries are all completed on-chain via stablecoins, "Treasury" will naturally equate to "Digital Asset Treasury." In this scenario, the purpose of DAT is no longer to obtain "amplified Bitcoin exposure," but to maintain the most basic cash flow operations of the enterprise. Companies unable to manage on-chain balance sheets will be like companies without bank accounts today, unable to participate in mainstream commercial activities.

(2) Re-evolution of the meaning of "Reserve"

- RWA becomes the new cash equivalent Under this trend, "cash and cash equivalents" may appear in new forms, such as deposit tokens, tokenized treasury bills, etc. RWA is no longer an experimental allocation but a foundational asset for daily financial operations.

- BTC becomes the ultimate reserve asset of the on-chain financial system Transforming from "hedging against fiat depreciation" to "hedging against on-chain dollar (stablecoin) risk." BTC will play a role similar to gold reserves for modern central banks: neutral, censorship-resistant, cross-border, and the lowest-layer "hard asset" of the on-chain financial system. Allocating a portion of the balance sheet to BTC will become a standardized financial strategy for enterprises.

(3) Universalization of the "Capital Structure Flywheel"

The "Capital Structure Flywheel" described in this report (buying scarce assets through debt financing to amplify the balance sheet) is no longer the patent of pioneers like MicroStrategy. As treasuries become fully on-chain: all listed companies will use on-chain assets (BTC, ETH, RWA) to prove their transparency and asset quality to the global capital market; enterprises will universally use on-chain assets as a basis for financing, refinancing, and market value management; the combination of stablecoins and on-chain assets will become the new core variable for global enterprises to compete for capital cost, financing efficiency, and market valuation.

In this endgame picture, DAT leaps from "strategy" to "infrastructure," from a breakthrough by a few pioneers to a necessary capability for all enterprises. The on-chain balance sheet will become the universal language of the global business system, and enterprises that master DAT will occupy a structural advantage in the future competitive landscape.