The New Order of On-Chain Capital: The Compliance Game between Deposit Tokens and Stablecoins

04/01/202602:37:47

As Real World Assets (RWA) bring trillions of dollars of traditional assets on-chain, the market demand for settlement currencies is undergoing deep stratification. For a long time, stablecoins like USDT and USDC have dominated the crypto market due to high liquidity. However, when facing institutional-grade RWA transactions, their limitations in "Capital Efficiency (Yield Generation)" and "Credit Safety (Insurance/Backstop Mechanisms)" are becoming increasingly apparent, failing to meet the stringent requirements of traditional financial institutions.

This report delves into the rise of commercial bank-led "Deposit Tokens" and analyzes the landmark event of December 2025, where the US OCC granted federal bank charters to crypto giants (Circle, Ripple, Paxos). It reveals a potential "Dual-Track Fusion" trend in the future digital currency market.

Bifu Research Team believes that the future RWA settlement system will no longer be dominated by a single currency. Instead, a stratified market structure is forming: the retail sector will continue to rely on highly liquid stablecoins, while the institutional sector will embrace interest-bearing deposit tokens. Meanwhile, regulated stablecoin issuers with federal charters are filling the gap between the two, accelerating their evolution towards "quasi-bank" entities through "Full Reserve + Federal Regulation" mechanisms.

I. Reconstructing the Money Spectrum: From "Bi-Polar" to "Tri-Polar"

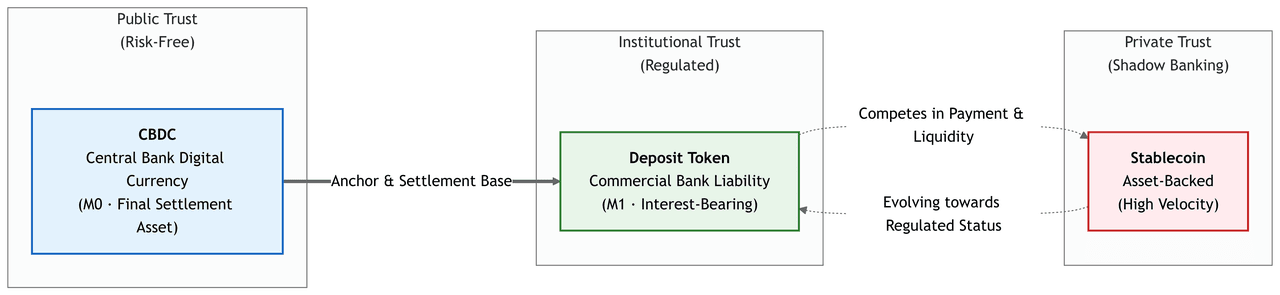

In traditional crypto narratives, digital currency is often simplified into a dichotomy of "Central Bank Digital Currency (CBDC)" vs. "Stablecoins." However, with the deepening of RWA, an intermediate form—Deposit Tokens—which aligns better with traditional financial logic and bridges traditional bank balance sheets with blockchain technology, is reshaping this spectrum.

The "Impossible Trinity" and Stratification of Digital Money

The current digital money ecosystem has evolved into three distinct dimensions, each solving market pain points at different levels:

On the left side of the spectrum is CBDC. As the ultimate anchor of trust in the financial system (M0), CBDC in the RWA context mainly plays the role of a Final Settlement Asset at the wholesale level. Central banks primarily intend for it to be used for large-value interbank transfers and settlements, rather than directly serving end-users for daily payments.

On the right side of the spectrum are Traditional Stablecoins. These "shadow bank" currencies based on asset reserves have established dominance in retail payments, high-frequency trading, and public chain DeFi markets due to their permissionless access and high cross-chain liquidity.

Currently, the most spotlighted asset occupying the middle ground is the Deposit Token. Essentially, it is a digital representation of commercial bank deposits on blockchain. Holding a deposit token implies a direct claim against the bank, allowing it to inherit the commercial bank's credit system directly. It is strictly subject to bank capital adequacy and liquidity regulations, making it the preferred compliant channel for institutions entering Web3.

Core Differentiation Analysis

For institutional investors, the key to distinguishing "Deposit Tokens" from "Stablecoins" lies not in the underlying blockchain technology, but in their legal nature and balance sheet structure.

Dimension | Deposit Token | Asset-Backed Stablecoin |

Issuer | Licensed Commercial Banks (e.g., JPM, HSBC) | Tech Firms/Non-Bank Financial Institutions (e.g., Tether) |

Legal Nature | Bank Liability (Deposit Certificate) | Beneficial Interest (Trust/Collateral) |

Yield | Interest-Bearing (Pays deposit interest) | Usually Non-Interest Bearing (Issuer retains yield) |

Regulatory Framework | Banking Law, Capital Adequacy, LCR | Payment Acts, Reserve Transparency |

Safety Net | Covered by Deposit Insurance (e.g., FDIC) | Relies on Asset Segregation & Audits |

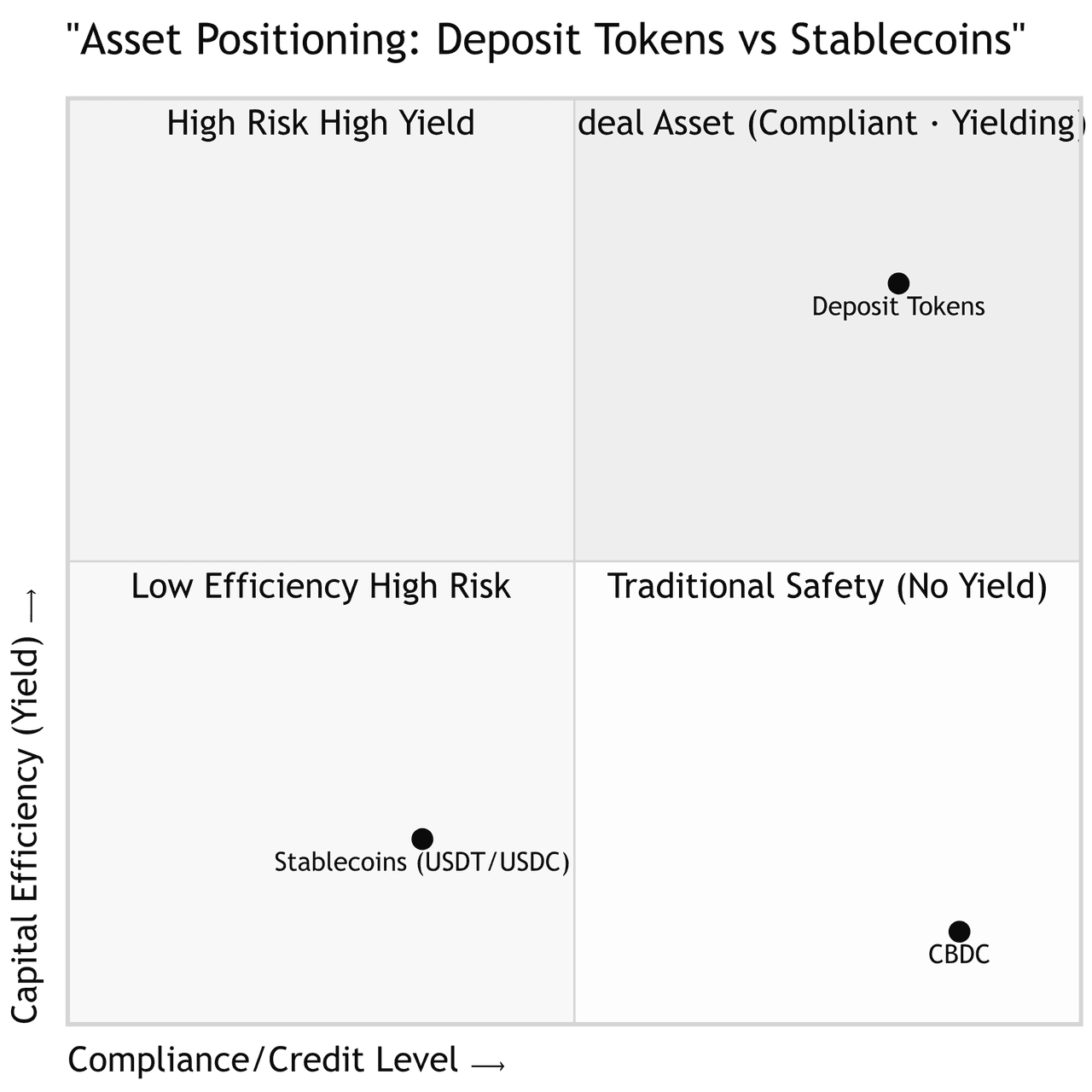

The quadrant chart below clearly shows the positioning of the three core assets in the digital currency ecosystem. We can see that Deposit Tokens are the only asset class occupying the "High Compliance + Interest-Bearing" advantage (Quadrant 1), which is key to attracting institutional capital. Stablecoins, while dominant in liquidity, are still playing catch-up in capital efficiency and compliance depth. CBDC, as a pure risk-free asset, offers the highest safety but lacks commercial yield.

II. Institutional Desire: Why Does RWA Need a "Third Currency"?

When asset management giants like BlackRock and Fidelity began attempting to trade treasuries or private credit on-chain, they found that the existing stablecoin system could not meet two core demands: Maximizing Capital Efficiency and Minimizing Counterparty Risk.

Refusing Idle Capital: A Revolution in Capital Efficiency

In the current DeFi model, institutions face significant opportunity costs. If an institution holds $100 million in USDC waiting to purchase RWA assets, this capital typically generates zero yield during the settlement period (T+1 or T+2). All interest income (mainly from the stablecoin issuer's treasury reserves) is retained by the issuer rather than distributed to the user.

The "Interest-Bearing" attribute of Deposit Tokens represents a paradigm shift in efficiency. Since their legal nature is bank deposits, deposit tokens inherently have the legal basis to pay interest. Through smart contracts, banks can implement "per-second interest calculation" or "conditional interest." For institutional treasuries managing billions in positions, the ability to convert idle funds into interest-bearing assets is the fundamental driver for reconstructing liquidity management via blockchain.

Reducing Counterparty Risk: Bank-Grade Credit Backstop

For traditional financial institutions, the core obstacle hindering the large-scale use of stablecoins has always been uncontrollable Counterparty Risk. Deposit tokens solve this problem through institutional design:

First, Deposit Insurance provides institutional security. As long as the issuer is a compliant commercial bank, deposit token holders enjoy deposit insurance protection (such as FDIC in the US). This is a credit endorsement that no non-bank stablecoin relying on commercial audit reports can offer.

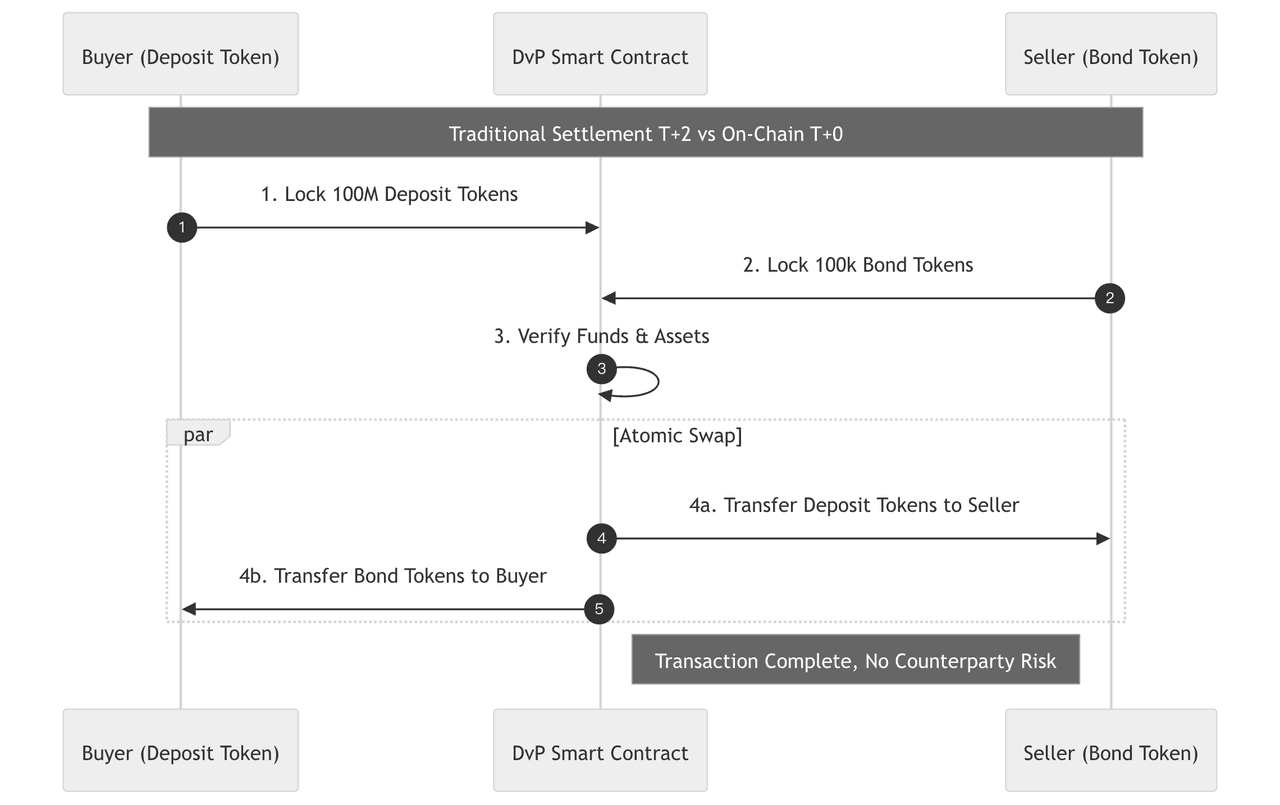

Second, Atomic Settlement (DvP) gains a compliant trust basis. In permissioned/consortium chain environments, deposit tokens possess robust KYC/AML pass-through capabilities, making them the only "large-value atomic settlement" tool accepted by regulators. They retain the instant settlement advantage of blockchain ("delivery versus payment") while eliminating the compliance risks associated with anonymous funds.

III. Global Sandbox and New Variables: The "Bankification" of Stablecoins

Market evolution is not solely driven by commercial banks. By the end of 2025, with the relaxation of US regulatory policies, crypto-native giants began to counterattack by obtaining "Federal Bank Charters," forming a unique competitive landscape with traditional banks.

The Counterattack of Traditional Giants (Commercial Bank Camp)

Commercial banks are accelerating their layout through differentiated paths. JPMorgan, relying on the Kinexys (formerly Onyx) network, not only runs JPM Coin on a private chain but also begins attempting to connect to public chains through cross-chain interoperability protocols, aiming to solve liquidity management problems for large multinational corporations globally.

HSBC has placed strategic emphasis on Corporate Treasury. It has successfully tested cross-bank transfers of tokenized deposits, aiming to help enterprises achieve 24/7 real-time fund allocation rather than simple payment functions. Meanwhile, the Bank of Korea's "Project Hangang" explores the application of deposit tokens in retail payments and emphasizes the seamless docking capability between commercial bank tokens and central bank wholesale CBDCs.

The Crypto-Native Resurgence (Compliant Stablecoin Camp)

In December 2025, the US Office of the Comptroller of the Currency (OCC) approved institutions like Ripple, Circle, and Paxos to transform into "National Trust Banks." This milestone event marks stablecoin issuers breaking through the "tech company" identity limitation and evolving towards a "quasi-bank" form.

Although these chartered institutions do not possess the lending capabilities of full-service commercial banks, their tokens, backed by "Full Reserve + Federal Regulation," have approached deposit tokens in safety. This model offers unique competitive advantages:

- Federal Regulatory Recognition: Enterprises break free from the limitations of state-level licenses (such as New York's BitLicense) for nationwide operations, obtaining federal regulatory status comparable to JPMorgan.

- Ultimate Safety: The full reserve model, while limiting their ability to pay interest (unable to profit from interest rate spreads like commercial banks), grants them higher liquidity safety than commercial bank deposits, theoretically eliminating run risks.

This essentially represents a successful breakout by crypto-native companies through "Self-Bankification" against the moats of traditional banks.

IV. Infrastructure Challenges: From "Islands" to "Interconnection"

As commercial banks and compliant institutions issue their own tokens, the market faces a new risk of fragmentation—"The Island Problem." If Citibank's tokens can only circulate within the Citi network and JPMorgan's tokens only on Kinexys, the vision of "Global Unified Liquidity" on blockchain will be difficult to realize.

Interoperability and the Unified Ledger

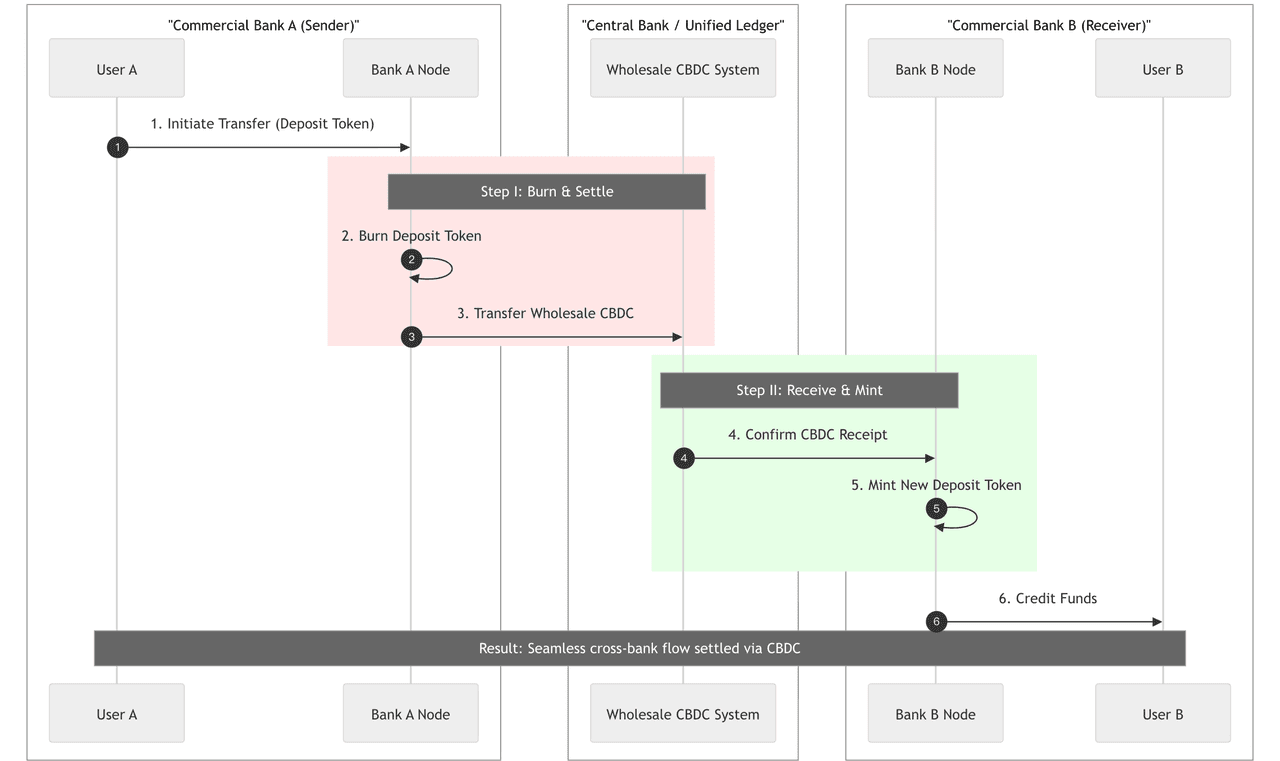

Consensus on solving this problem is coalescing around the "Unified Ledger" concept. As advocated by the Bank for International Settlements (BIS), the industry needs to build a public infrastructure containing central bank money, commercial bank deposits, and tokenized assets. In this architecture, Wholesale CBDC will play a key bridging role: in cross-bank settlement, Bank A burns deposit tokens, transfers CBDC to Bank B, and Bank B mints new deposit tokens for the recipient, achieving seamless circulation.

Balancing Privacy and Compliance

Furthermore, institutional transactions often involve highly sensitive commercial secrets. How to maintain on-chain transparency (for automated auditing) while protecting transaction privacy is another major challenge for infrastructure construction. Privacy computing technologies such as Zero-Knowledge Proofs (ZKP) are expected to play a key role in the compliance layer of deposit tokens, ensuring data is "usable but invisible."

V. Outlook: Dual-Track Parallelism and the Exchange's New Mission

Regulatory Convergence: "Same Risk, Same Rules"

The Evolution of Exchange Roles: Connection and Empowerment

Building a New Order for Intelligent Capital

The emergence of deposit tokens fills the long-missing "Institutional Puzzle Piece" in the RWA landscape. It is not meant to eliminate stablecoins, but to pave a high-speed highway into Web3 for the trillions of dollars of traditional capital that demand extreme efficiency and safety. With the full entry of commercial banks and the "bankification" transformation of crypto giants, a clearly stratified and interconnected new order of on-chain capital is forming. In this new order, money is no longer just a payment tool, but a programmable, interest-bearing intelligent asset.

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.