Digital Finance New Infrastructure: Hong Kong's Path to RWA Market Breakthrough and Investment Opportunities

20/01/202603:20:06

Bifu Research | 2026

Abstract

In the critical cycle where the global digital asset market is shifting from "wild growth" to "compliance and implementation," Hong Kong, China, with its unique financial infrastructure and forward-looking regulatory framework, is becoming a core testing ground for global RWA (Real World Asset) tokenization. Unlike the early on-chain native explorations of DeFi, the Hong Kong model demonstrates distinct characteristics of being "institution-led" and "industry-supported."

This report deeply analyzes the policy dividends, dual-track regulatory architecture, and typical practical cases of the Hong Kong RWA market. Bifu Exchange believes that with Project Ensemble entering the practical phase and the enactment of the "Stablecoin Ordinance," Hong Kong is poised to become the premier hub connecting high-quality industrial assets in the Greater Bay Area with global Web3 liquidity. This also presents massive asset-side opportunities for compliant trading platforms.

I. Hong Kong RWA: The Advantage of Timing and Location

1.Policy Direction: From "Declaration" to "Implementation"

Since the release of the "Policy Statement on Development of Virtual Assets in Hong Kong" in 2022, the Hong Kong government's support for Web3 has shifted from slogans to substantive financial infrastructure. Unlike the ambiguous regulatory attitudes in some regions, the HKSAR government clearly proposed the strategic policy of "using the virtual to support the real," viewing RWA as a key tool to improve traditional financial efficiency and reduce financing costs.

The certainty of this "top-level design" is the biggest dividend of the Hong Kong market. The government has not only launched the "Digital Bond Grant Scheme" (subsidizing up to HKD 2.5 million per issuance) but also cleared obstacles through legislation. For investors, this means RWA assets in Hong Kong are no longer experimental products in a gray area, but financial products strictly protected by law.

2.The Connector Role: Backed by the Greater Bay Area, Facing the World

Hong Kong is not only an international financial center but also the "Super Connector" of the Greater Bay Area (GBA).

- Asset Side: Backed by the mainland's massive new energy (photovoltaic, charging piles), high-end manufacturing, and supply chain assets. These high-quality industries urgently need to access global capital markets through RWA.

- Capital Side: Aggregates global Web3 capital and traditional Family Office funds seeking stable returns.

We believe that the core competitiveness of Hong Kong RWA lies in the "depth of the asset side." Hong Kong has the capability to use digital means to transform China's high-quality supply chain assets into investment targets with stable cash flows.

II. Security and Trust Brought by Dual-Track Regulation

Hong Kong's regulatory framework for RWA is clear and highly operable, primarily driven by a dual-track system involving the Securities and Futures Commission (SFC) and the Hong Kong Monetary Authority (HKMA). Although this rigorous architecture raises the entry barrier, it greatly eliminates compliance risks and provides security guarantees for market participants.

1.SFC: Compliance Definition of Security Tokens

The SFC defines most RWAs as "Tokenized Securities." This means:

- Legal Certainty: On-chain tokens represent the real ownership of off-chain assets and are protected by Hong Kong law.

- Intermediary Responsibility: Issuers and trading platforms must undertake due diligence responsibilities similar to traditional securities brokers.

2.HKMA: "Stablecoin Ordinance" Officially in Effect

The HKMA has taken a critical step in the compliance of fund flows. The "Stablecoin Issuer Regulatory Regime" officially came into effect on August 1, 2025.

- Licensing Management: Fiat stablecoin issuers must obtain a license in Hong Kong, ensuring full backing by asset reserves.

- Payment Loop: The emergence of compliant stablecoins thoroughly bridges the "last mile" of RWA asset dividend distribution and settlement, eliminating investor concerns about fiat on/off ramps.

3.Policy Breakthrough: Staking Services Unbanned

In September 2025, the SFC and HKMA issued a joint circular officially permitting compliant intermediaries to provide virtual asset Staking services to clients. This policy breakthrough is profound for the RWA market, meaning that some interest-bearing assets can design yield structures more flexibly. It also provides Bifu and other platforms with more diverse space for product innovation.

In this high-standard regulatory environment, trading platforms that can operate compliantly in Hong Kong or follow Hong Kong standards will naturally possess higher credit endorsements and more easily gain the trust of traditional institutional investors.

III. Infrastructure and Ecosystem Map

Hong Kong is building a "financial-grade" RWA protocol stack distinct from the public chain ecosystem.

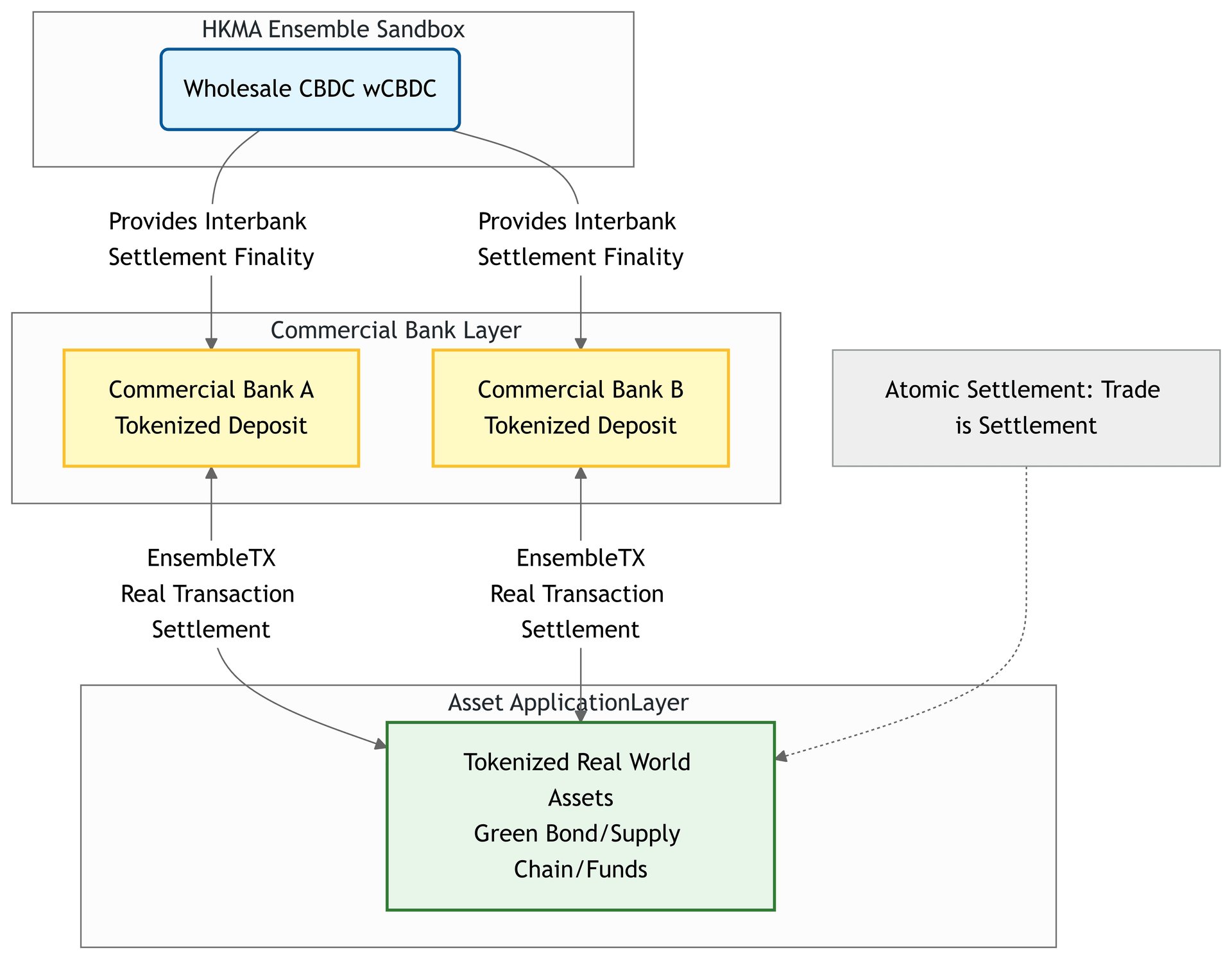

1.Core Infrastructure: Project Ensemble and EnsembleTX

Project Ensemble is the HKMA's core financial infrastructure project. In November 2025, the HKMA officially launched EnsembleTX, marking the project's transition from sandbox testing to the "real transaction" pilot phase.

1.1 Core Mechanism: wCBDC and Atomic Settlement

Unlike retail CBDC used by individuals, the core of Project Ensemble is to establish a blockchain-based wCBDC (wholesale CBDC) sandbox.

- Hub Function: wCBDC serves as the final settlement asset, supporting interbank transfers of "Tokenized Deposits" issued by commercial banks.

- Risk Elimination: Through smart contracts, tokenized assets (such as Bond RWA) and tokenized funds can achieve Atomic Settlement (i.e., "Delivery vs Payment"), ensuring that transactions are either completed simultaneously or cancelled simultaneously, thoroughly solving the counterparty risk of the T+2 settlement cycle in traditional finance.

1.2 Architecture Working Group and Four Main Themes

The HKMA established the Project Ensemble Architecture Working Group, with members including HSBC, Standard Chartered, BOC Hong Kong, HashKey Group, Ant Digital, etc. The sandbox testing focuses on four main themes:

- Fixed Income and Investment Funds: Bond issuance, distribution, and secondary market trading.

- Liquidity Management: Interbank fund transfers and treasury management.

- Green and Sustainable Finance: Digitization and certification of green bonds and carbon credits.

- Trade and Supply Chain Finance: Utilizing blockchain technology to solve multi-party trust issues, which is also a sector Bifu focuses on for real economy empowerment.

2.Typical Practical Cases

- Government Green Bond (Project Evergreen):

- Latest Progress: In November 2025, the Hong Kong government successfully issued the third batch of digital green bonds, totaling approximately HKD 10 billion, covering HKD, RMB, USD, and EUR.

- Significance: This proves that Hong Kong possesses the capability for large-scale, normalized issuance of multi-currency digital bonds, validating the maturity of the legal framework.

- Tykhe Capital: Launched a real estate fund token (STO) for professional investors, providing a commercial sample for the securitization of illiquid assets.

IV. Market Outlook and Bifu's Observations

With the perfection of infrastructure, the Hong Kong RWA market is on the eve of an explosion. We predict the market will show the following three major trends, which align highly with Bifu Exchange's long-term strategic layout.

1.Trend 1: Diversification and Quality Upgrade of Asset Classes

The market will expand from single Treasury RWAs to industrial assets with greater yield potential. Blockbuster RWA products will successively appear in real sectors like new energy infrastructure and cross-border trade finance. Bifu will continue to monitor such assets that possess real revenue-generating capabilities and clear cash flows, dedicated to screening high-quality targets that can traverse cycles for users.

2.Trend 2: The Hub Role of Trading Platforms Becomes Prominent

In the RWA industry chain, exchanges are no longer just matching venues but "Super Converters" connecting Web3 liquidity with compliant assets. Due to the specificity of RWA assets (e.g., dividend distribution, asset disclosure), trading platforms need to provide deeper post-investment management and information disclosure services. Bifu is committed to providing transparent, intuitive RWA asset dashboards through technological upgrades, allowing users to participate in RWA investment as conveniently as trading spot assets.

3.Trend 3: Gradual Release of Liquidity

With the advancement of the regulatory sandbox, the entry threshold for RWA products is expected to gradually relax from Professional Investors (PI) to Retail Investors (Retail), and secondary market liquidity will usher in a qualitative leap.

The rise of the Hong Kong RWA market is essentially a "New Infrastructure" movement in the financial industry. It is not about hyping concepts, but about using blockchain technology to make financial services serve the real economy at a lower cost and with greater transparency.

In this process, compliance is the biggest dividend. Bifu Exchange will always uphold the philosophy of embracing regulation and operating steadily, closely monitoring Hong Kong's RWA policy dynamics and high-quality asset-side opportunities, witnessing the golden age of the integration of digital finance and the real economy together with investors.

V. References

To ensure the accuracy and timeliness of information, the regulatory framework details cited in this article are based on official documents from relevant regulatory bodies in Hong Kong, China. For in-depth research, it is recommended to visit the following official thematic pages:

FSTB (2022):

https://www.info.gov.hk/gia/general/202210/31/P2022103100218.htm

HKMA (2024):

https://www.hkma.gov.hk/eng/news-and-media/press-releases/2024/08/20240828-3/

HKMA (2024):

SFC (2023):

https://apps.sfc.hk/edistributionWeb/gateway/EN/circular/doc?refNo=23EC52

HKMA (2024):

https://www.hkma.gov.hk/eng/news-and-media/press-releases/2024/07/20240717-3/

HKMA (2024):

https://www.hkma.gov.hk/eng/news-and-media/press-releases/2024/02/20240207-3/

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.