Singapore RWA Practical Guide (Part I): The "Red Lines" and "Green Zones" of Asset Tokenization

19/12/202506:39:36

In November 2025, the Monetary Authority of Singapore (MAS) released an updated Guide on the Tokenisation of Capital Markets Products. This document not only reiterates the "technology-neutral" regulatory principle but also defines the attributes of Real World Assets (RWA) under Singapore's legal framework through 17 specific case studies.

As a leading global digital asset trading platform, Bifu consistently monitors regulatory dynamics to safeguard user interests. This report, the first in a series, focuses on the "Asset Side", providing an in-depth analysis of how MAS defines security tokens versus non-security tokens. For investors and project owners, understanding these definitions is the first step in identifying high-quality assets and avoiding compliance risks.

I. Core Principle: Ending Ambiguity, Returning to "Economic Substance"

In the early stages of Web3 development, many projects attempted to circumvent traditional financial regulations by creating new terms (e.g., "Governance Tokens," "Utility Tokens"). However, MAS has explicitly broken this ambiguity in the new guide.

The core logic of Singapore's regulation can be summarized as: "Same Activity, Same Risk, Same Regulatory Outcome."

This means that when determining whether a token falls under regulated "Capital Markets Products" (CMPs), MAS looks beyond the underlying blockchain technology or the terminology used in a whitepaper. Instead, it conducts a Holistic Assessment, focusing on the Economic Substance of the token.

In short, if it looks like a duck, swims like a duck, and quacks like a duck, then in the eyes of the regulator, it is a duck—regardless of whether it is minted as an NFT or an ERC-20 token.

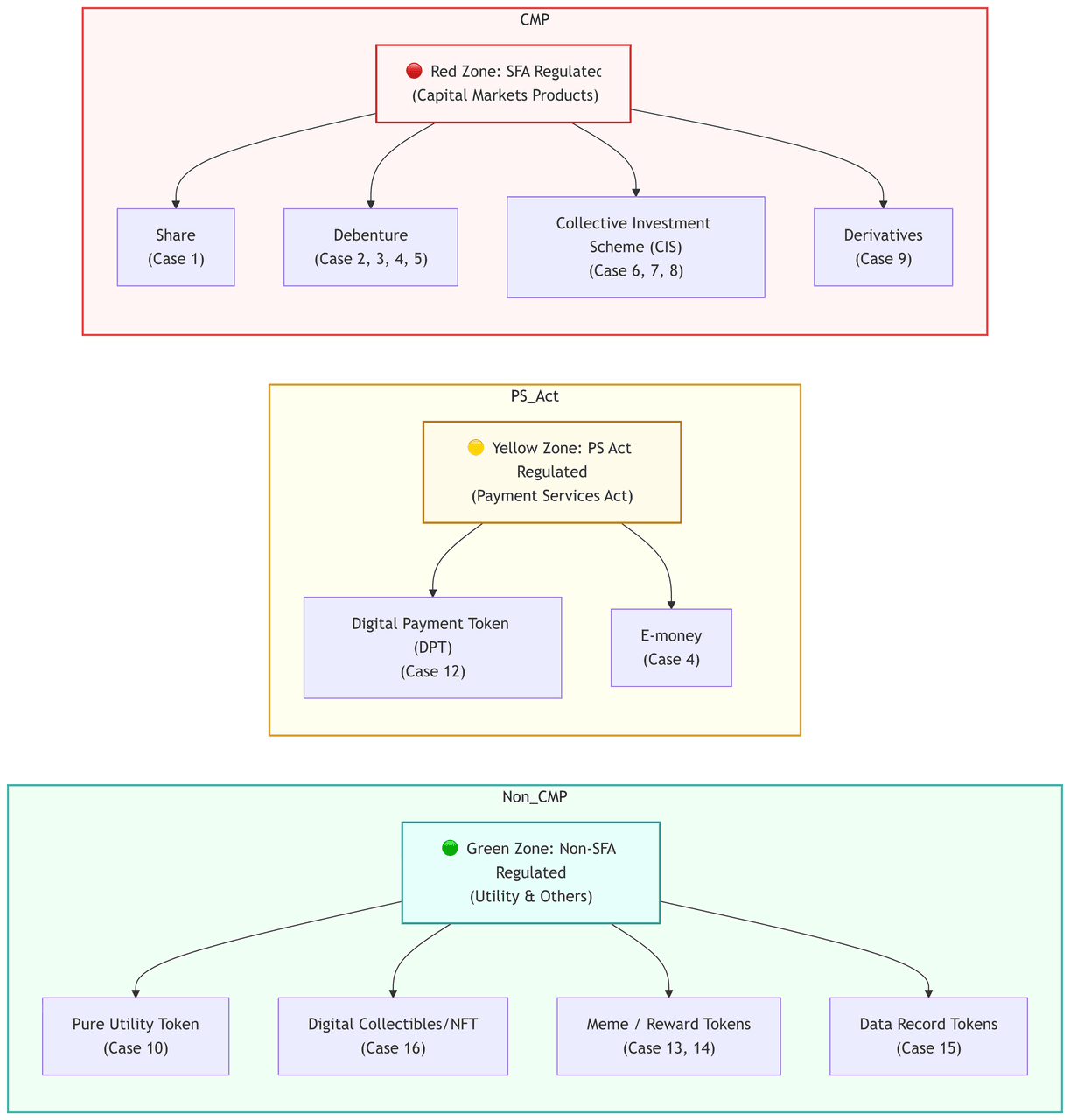

II. Regulatory "Red Lines": Which RWAs are Capital Markets Products (CMPs)?

Under the Securities and Futures Act (SFA) of Singapore, Capital Markets Products (CMPs) include securities, units in a Collective Investment Scheme (CIS), and derivatives contracts. Once a token falls into this category, its issuance must comply with strict regulations, including prospectus requirements and licensing.

The MAS Guide delineates three key areas of focus through case studies, which are currently the areas in the RWA sector most prone to crossing compliance red lines.

Debentures: Not All "Lending" is Just DeFi

In the RWA sector, bond tokenization is one of the most common forms. MAS explicitly points out that if a token represents the issuer's evidence of indebtedness or obligation to repay the holder, the token constitutes a Debenture.

- Typical Scenario A (Lending Platform - Case 2): A project sets up a Special Purpose Vehicle (SPV) to raise funds from investors, promising future repayment of principal and interest. Even if this process is executed automatically via smart contracts, the token is still considered a debenture.

- Typical Scenario B (Buyback Promise - Case 3/4): Some projects issue so-called "Membership Tokens" but promise to buy back the tokens at a fixed price under certain conditions. This "buyback obligation" constitutes a liability for the issuer in legal terms; thus, the token is highly likely to be classified as a debenture.

Bifu's View: For investors seeking stable returns, it is crucial to identify whether a clear legal debt relationship exists behind the token. Compliant debenture tokenization can provide investors with legal repayment guarantees, rather than relying solely on code-based trust.

Collective Investment Schemes (CIS): The "Deep Water" of Tokenization

This is the area most prone to misunderstanding in RWA innovation. Many projects attempt to "fractionalize" physical assets such as real estate, gold, or art on-chain.

According to MAS Case 7, if the following characteristics are met, the token is likely considered a Collective Investment Scheme (i.e., a Fund):

- Pooling of Funds: Investors' funds are pooled together.

- Centralized Management: The underlying assets (e.g., gold storage, property operation) are managed by the project owner (or a third party), with no day-to-day management participation by investors.

- Profit Sharing: Investors' returns are derived from profits or capital appreciation of the managed assets.

Case Implication: Even if a project claims the token is merely a "Gold Ownership Certificate," if investors cannot physically redeem the gold and instead rely on the project owner to manage the vault and distribute profits, this constitutes a fund offering under Singapore law. This means the issuer must hold a fund management license (LFMC/RFMC) and comply with strict asset custody requirements.

Equities and Derivatives

- Shares (Case 1): If a token confers ownership interests, dividend rights, or voting rights (regarding corporate matters) to the holder, it clearly constitutes a Share.

- Derivatives (Case 9): If the token's price performance is directly pegged to the stock price of a listed company and the issuer has an obligation to settle based on that price, the token is considered a "Securities-based Derivatives Contract", even if the holder does not genuinely hold the underlying stock.

III. Innovation "Green Zones": Which Assets Are Not Securities?

MAS regulation aims not to stifle innovation but to clarify boundaries. The Guide also lists cases not considered CMPs, leaving room for non-financial Web3 innovation.

Utility Tokens

If a token is used solely to access certain services or computing power and does not represent a claim on the issuer's debt or equity, it generally does not constitute a security.

- Case 10: A platform issues tokens used solely to pay for cloud computing power rentals. The token has no dividend rights and no buyback promise. Such tokens are not within the scope of SFA regulation.

Digital Collectibles and NFTs

MAS confirms that pure Digital Collectibles typically do not fall under financial regulation.

- Case 16: Tokens representing unique digital characters (NFTs) used only for collection, gaming, or community access. The issuer does not promise token appreciation nor market it as an investment product. Such assets fall under consumer goods, not financial products.

Other Non-Security Assets

- Meme Coins (Case 14): Used solely for entertainment or speculation, with no intrinsic utility or financial promise, not considered a CMP.

- Reward Tokens (Case 13): Issued solely as rewards for user behavior, involving no fundraising, not considered a CMP.

- Data Records (Case 15): Used solely to immutably record data (e.g., environmental monitoring data for green bonds). The token itself contains no bond rights and is not considered a CMP.

(Figure Note: Overview of Regulatory Classification for 17 Token Cases in the MAS Guide.Case 11 (consulting services) and Case 17 (overseas issuance) are not included in the token classification, but are also subject to relevant regulations.)

IV. Exemptions: Compliance Paths for CMPs

Being classified as a security (CMP) does not mean one must undergo a complex public offering process. According to the MAS Guide (Section 3.4), issuances meeting one of the following conditions may be exempt from Prospectus requirements:

- Small Offers: Total funds raised do not exceed SGD 5 million within any 12-month period.

- Private Placement: Offers made to no more than 50 investors within any 12-month period.

- Institutional/Accredited Investors: Offers made solely to qualified institutions or high-net-worth individuals.

Bifu's Note: This means that early-stage RWA projects or products targeting specific client groups still have flexible and compliant survival space.

V. Conclusion: Compliance is the Cornerstone of Asset Value

The Guide released by MAS provides a high-standard reference frame for the global RWA market. For the industry, this marks the transition of RWA from the "Proof of Concept" phase to the "Institutional Application" phase.

As a bridge connecting traditional finance and the digital economy, Bifu Exchange adheres to strict screening standards on the asset side:

- Substantive Review: When evaluating RWA projects, we look beyond the technical whitepaper. We collaborate with legal teams to review the legal structure of the underlying assets based on the "Economic Substance" principle akin to MAS.

- Compliance Disclosure: For RWA assets classified as securities, we require project owners to provide complete compliance proofs and risk disclosure documents to ensure user awareness.

- Risk Isolation: We are committed to introducing projects with clear structures and definite asset rights, providing comprehensive safeguards for investors' assets.

We believe that increased regulatory clarity will benefit the long-term development of the RWA sector. It will help the market eliminate inferior supply, allowing quality assets with genuine business value and legal protection to stand out.

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.

Reference: https://www.mas.gov.sg/regulation/guidelines/guide-on-tokenisation-of-cmps