EU Digital Finance "Three Pillars" Regulatory Panorama: New Compliance Paths for RWA

14/01/202607:32:41

Executive Summary

As the global crypto-asset market matures, the European Union (EU), through its forward-looking "Digital Finance Package," is building the world's most systematic digital asset regulatory infrastructure. Unlike some regions that focus on "regulation by enforcement," the EU is committed to establishing clear ex-ante access and operational standards.

This report provides an in-depth analysis of the three core pillars constituting this system: Markets in Crypto-Assets Regulation (MiCA), DLT Pilot Regime, and Digital Operational Resilience Act (DORA). Our research suggests that this combination, by clarifying asset attributes, innovating trading and settlement mechanisms, and strengthening technical risk control standards, is removing legal barriers to the mass adoption of Real World Assets (RWA). For market participants, understanding this framework is key to seizing the next wave of institutional dividends.

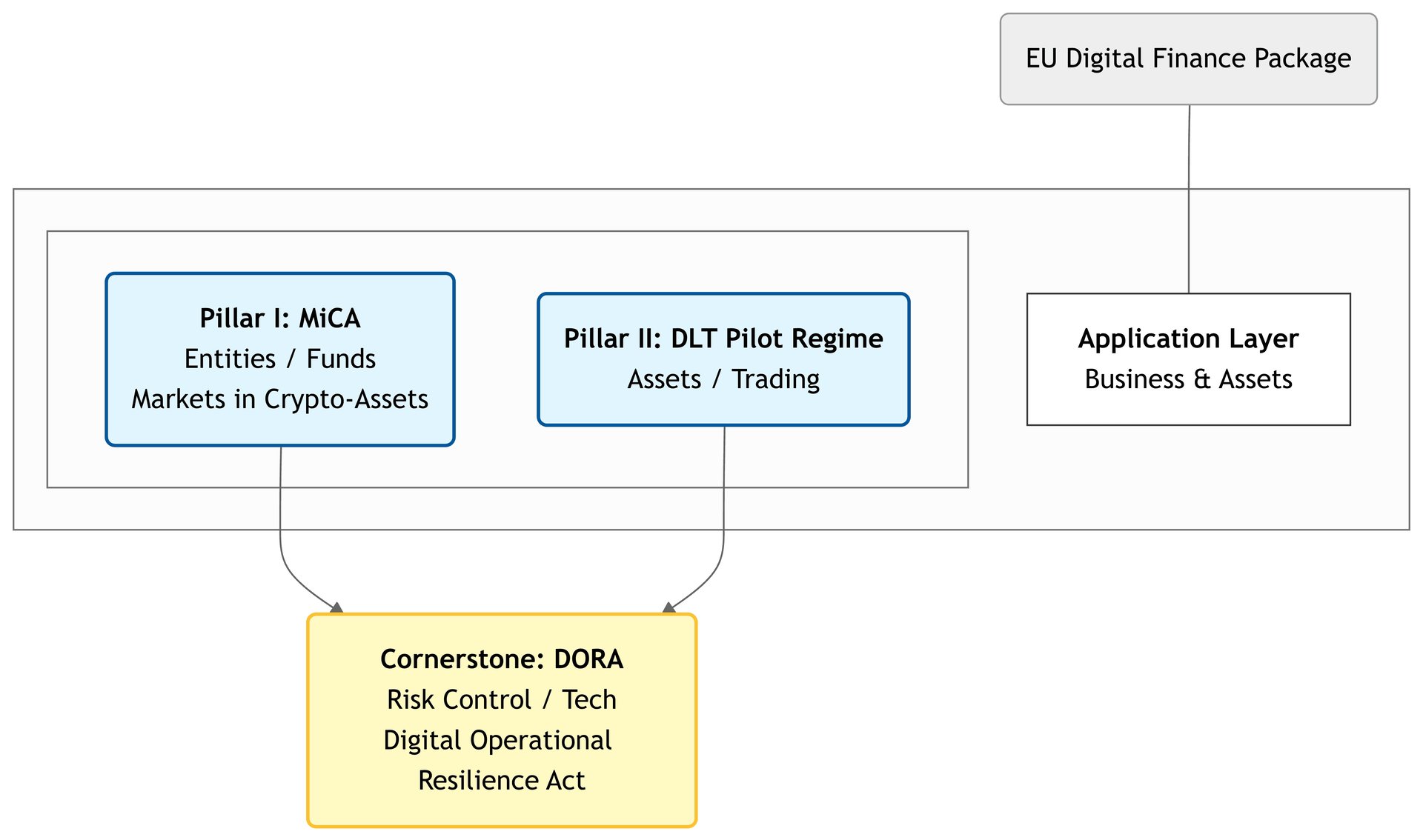

1.Regulatory Background: From Single Regulation to Ecosystem Loop

In recent years, the market has often focused on MiCA. However, for RWA—a special field merging traditional financial assets with blockchain technology—a single regulation is insufficient to cover its full scope. The EU's current regulatory logic presents a rigorous "trinity" structure, systematically regulating market entities, asset issuance, and technical security respectively.

The core intent of this system is to balance financial innovation with systemic risk, attempting to introduce traditional capital market liquidity into the on-chain world while safeguarding investor rights.

2.MiCA: Building RWA Infrastructure and Funding Channels

Markets in Crypto-Assets Regulation (MiCA) is the cornerstone of the EU's digital finance strategy. Its impact on the RWA track is mainly reflected in regulating trading settlement tools and establishing service provider standards.

2.1 Standardization of Stablecoins and Settlement Mechanisms

In RWA business, achieving "Delivery vs Payment" (DvP) and atomic settlement relies on on-chain fiat carriers. MiCA has established strict issuance and reserve standards for stablecoins (referred to as "Asset-Referenced Tokens - ARTs" and "E-Money Tokens - EMTs" in the regulation).

Notably, MiCA stipulates that in regulated RWA trading scenarios, settlement tools should primarily be E-Money Tokens (EMTs) issued by Electronic Money Institutions (EMIs) or credit institutions (banks), pegged to a single fiat currency. This regulation includes the following core constraints:

- Transaction Cap for Non-Euro Tokens: To maintain Euro monetary sovereignty, MiCA stipulates that if a non-Euro denominated ART or EMT exceeds 1 million transactions OR a daily transaction value of 200 million Euros as a "Means of Exchange" within the Eurozone, the issuer must stop issuance and take reduction measures. This means Euro stablecoins will dominate large-scale RWA settlement scenarios.

100% Reserve Requirement: EMT issuers must hold fiat reserves at least equal to the face value of the circulating tokens, and these reserves must be safeguarded in independent credit institutions, ensuring users have a 1:1 right of redemption at any time.

2.2 Access for Crypto-Asset Service Providers (CASP)

The core link of RWA lies in the verification of off-chain assets and the custody of on-chain tokens. MiCA mandates that relevant service providers (CASPs) must be licensed and sets specific capital thresholds:

- Minimum Capital Requirements: Different categories of service providers must meet different prudential capital requirements. For example, the minimum capital requirement for operating a trading platform is 150,000 EUR, while for custodians it is 125,000 EUR (or one-quarter of their fixed overheads, whichever is higher).

- Asset Segregation and Bankruptcy Protection: Custodians must strictly segregate client assets from their own assets legally and technologically. The regulation clarifies that in the event of a service provider's bankruptcy, custodial assets do not form part of the liquidation estate.

This arrangement removes the biggest concern for traditional large financial institutions entering the crypto market, laying the legal foundation for large-scale capital entry.

3.DLT Pilot Regime: The Innovation Sandbox for Security Assets

For RWA assets possessing "financial instrument" attributes (such as stocks, bonds, funds), the regulatory basis is not MiCA, but the more innovative DLT Pilot Regime. This regime aims to solve compatibility issues between existing securities laws (such as CSDR) and blockchain technology characteristics.

3.1 Integration of Trading and Settlement

In traditional financial markets, trading venues and settlement institutions must be legally separated, leading to settlement delays (usually T+2). The DLT Pilot Regime allows the establishment of a DLT Trading and Settlement System (DLT TSS). By exempting specific provisions of the Central Securities Depositories Regulation (CSDR), the legal level officially recognizes the "trading is settlement" capability brought by blockchain technology, significantly reducing counterparty risk and improving capital efficiency.

3.2 Scope and Size Limitations

To control potential risks during the pilot, the EU has set clear thresholds for the size of assets entering this sandbox. This also clearly outlines the development focus of RWA at the current stage—mainly focusing on small and mid-cap assets and corporate bonds.

Asset Class | Eligibility Thresholds | Notes |

Shares | Issuer Market Capitalization < 500 Million EUR | Applicable only to SME stocks |

Bonds | Issuance Size < 1 Billion EUR | Includes corporate bonds, securitized debt, etc. |

Funds (UCITS) | Assets Under Management (AUM) < 500 Million EUR | Limited to regulated UCITS funds |

In addition, regulators have set platform-level double risk control thresholds:

- 6 Billion EUR (Soft Cap): When the total market value of financial instruments recorded on the DLT infrastructure reaches 6 billion EUR, operators may not admit new financial instruments.

- 9 Billion EUR (Hard Cap): If the total market value exceeds 9 billion EUR, operators must initiate a transition strategy to orderly reduce business or migrate to traditional infrastructure.

This design indicates that the EU is adopting a "walk before you run" strategy, prioritizing support for SME financing and specific types of bond tokenization, with hopes of further relaxing restrictions once the technology is proven mature.

4.DORA: Strengthening Operational Resilience and Technical Standards

With the Digital Operational Resilience Act (DORA) fully coming into effect in early 2025, the technical threshold for the digital finance industry will rise significantly. DORA covers not only traditional banks but also all crypto-asset service providers.

4.1 Elevating ICT Risk Management Standards

RWA business usually involves complex on-chain and off-chain interactions. DORA requires relevant entities to establish a comprehensive Information and Communication Technology (ICT) risk management framework.

- Major Incident Reporting Timeline: Financial entities must establish extremely agile incident reporting mechanisms. Once a major ICT-related incident occurs, an initial notification must be submitted to the competent authority within 24 hours of awareness, and an intermediate report within 72 hours.

- Threat-Led Penetration Testing (TLPT): Significant financial entities must conduct a high-level, threat-intelligence-based penetration test (TLPT) at least every 3 years. This is no longer a simple code audit but a comprehensive combat drill covering social engineering and internal threats.

4.2 Strengthening Third-Party Risk Management and Penalties

DORA introduces direct oversight powers over "Critical ICT Third-Party Service Providers" (CTPPs, such as cloud providers, critical oracles).

- Proof of Control Capability: RWA projects must demonstrate their control capabilities and exit strategies regarding these external dependencies.

- Cost of Non-Compliance: For entities designated as Critical ICT Third-Party Service Providers, non-compliance can lead to periodic penalty payments of up to 1% of their average daily worldwide turnover, forcing technology providers to maintain extremely high compliance standards.

This will prompt RWA platforms to be more prudent when selecting technology partners, favoring those with mature architectures and high compliance degrees, thereby indirectly raising the security level of the entire ecosystem.

5.Market Outlook and Conclusion

Synthesizing the above three major regulations, we can clearly see the development trajectory of the EU digital finance market:

- Accelerated Institutionalization: With clear compliance paths, traditional financial institutions with deep compliance backgrounds and risk management capabilities will accelerate their layout in the RWA track, including issuing on-chain bonds or launching tokenized funds.

- Emergence of Compliance Premium: Platforms operating under the "Three Pillars" system, while bearing higher compliance costs, can provide users with higher levels of asset security and legal certainty. This "compliance premium" will become a core competitiveness.

- Upgrading Industry Standards: The implementation of DORA will force the industry to upgrade technical standards, reducing user asset losses caused by technical failures or hacker attacks, and promoting the industry's transition from wild growth to high-quality development.

For investors and market participants, paying attention to platforms and projects that actively embrace the regulatory framework and continuously invest in technical security and compliance will be a prudent choice in the new regulatory era. Bifu Exchange remains highly attentive to global regulatory dynamics and is committed to providing users with compliant, safe, and professional digital asset service experiences.

6.Official References

To ensure accuracy and timeliness, the regulatory framework details cited in this report are based on official documents from relevant EU regulatory bodies. For in-depth research, consulting the following legal texts and official interpretations is recommended:

Markets in Crypto-Assets Regulation (MiCA):

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32023R1114

DLT Pilot Regime:

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022R0858

https://www.esma.europa.eu/esmas-activities/digital-finance-and-innovation/dlt-pilot-regime

Digital Operational Resilience Act (DORA):

https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX%3A32022R2554

https://www.eiopa.europa.eu/digital-operational-resilience-act-dora_en

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.