Liquidity Breakout: Synthetic RWAs Open a New Chapter in Trading

04/02/202608:01:24

Bifu Research | 2026

Executive Summary

As the integration of blockchain technology and traditional financial systems enters deep waters, the Real World Asset (RWA) sector is undergoing a critical transition from simple "asset tokenization" to deeper "value discovery." Although the tokenization of government treasuries has achieved significant scale over the past two years, the majority of underlying assets still face the challenge of liquidity scarcity.

Bifu Research Institute believes that the RWA market is forming a dual-layer architecture: the bottom layer is the "Fundamental Asset Layer" centered on ownership confirmation and yield generation, while the top layer is the "Financial Trading Layer" centered on liquidity and speculation. We believe that the next growth point for RWAs will no longer be limited to holding static assets, but will involve introducing risk exposures of traditional financial assets into the crypto liquidity market through Synthetic Assets and Options Tools.

In this paradigm shift, Centralized Exchanges (CEXs), leveraging efficient clearing and settlement systems and unified margin mechanisms, will become the key hub connecting traditional financial volatility with crypto asset liquidity, greatly enhancing capital efficiency.

I. Introduction: From "Asset Onboarding" to "Efficiency Enhancement"

1.Market Status: Solid Foundation, Unsolved Puzzles

Looking back at 2024-2025, the RWA sector completed crucial infrastructure construction. Represented by Tokenized Treasuries, yield-bearing assets successfully brought risk-free returns from traditional finance on-chain, establishing a native benchmark interest rate for the DeFi world. The success of this phase proved the feasibility of combining legal frameworks with blockchain technology, establishing the legitimate status of "asset tokenization."

However, as exploration deepened, objective limitations of the physical world emerged. Most non-standard RWA assets (such as real estate, private credit, fine art) inherently possess characteristics of low-frequency trading, non-standardization, and complex settlement. This has led to the current "Holding is the End" phenomenon in the RWA market—capital often becomes stagnant after entry, lacking secondary market turnover and gaming.

Market capital actually exhibits distinct stratification: one part is Yield Seeking capital, whose needs are relatively well met by existing RWA products; the other part is Volatility/Alpha Seeking capital. The massive liquidity demand of this latter group has not yet been effectively captured by the RWA market.

2.Evolution Direction: Extension of Trading Scenarios

The next step in RWA evolution is not to negate "holding," but to layer "trading" on top of it. We need to use financial engineering to transform low-liquidity underlying assets into high-liquidity trading targets.

This is the mission of the "Financial Trading Layer": by introducing synthetic assets and derivative tools, it satisfies the market's demand for risk management, macro hedging, and price speculation, thereby activating stagnant capital and achieving the leap from "Asset Onboarding" to "Capital Efficiency Enhancement."

II. Path Selection: Symbiosis of Physical and Synthetic Assets

1.Complementarity of Two Models

In the future direction of RWA development, the physical asset model and the synthetic asset model will develop in parallel, complementing each other.

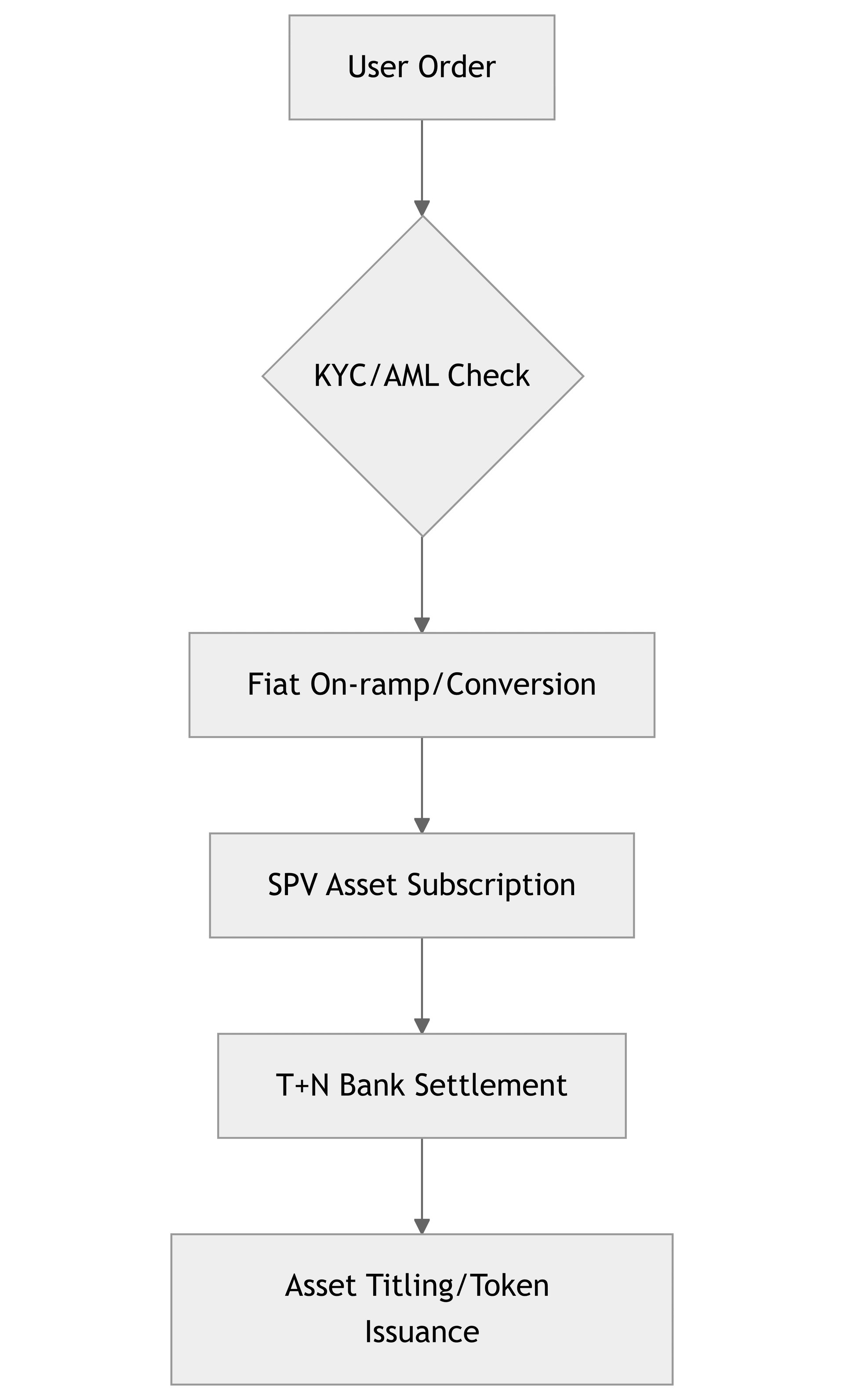

- Asset-Backed Model: Positioned for value storage and passive income. Its core lies in the rigor of legal ownership confirmation, suitable for long-term wealth management and treasury reserves. In this model, CEXs act more as distribution channels, helping high-quality assets reach users.

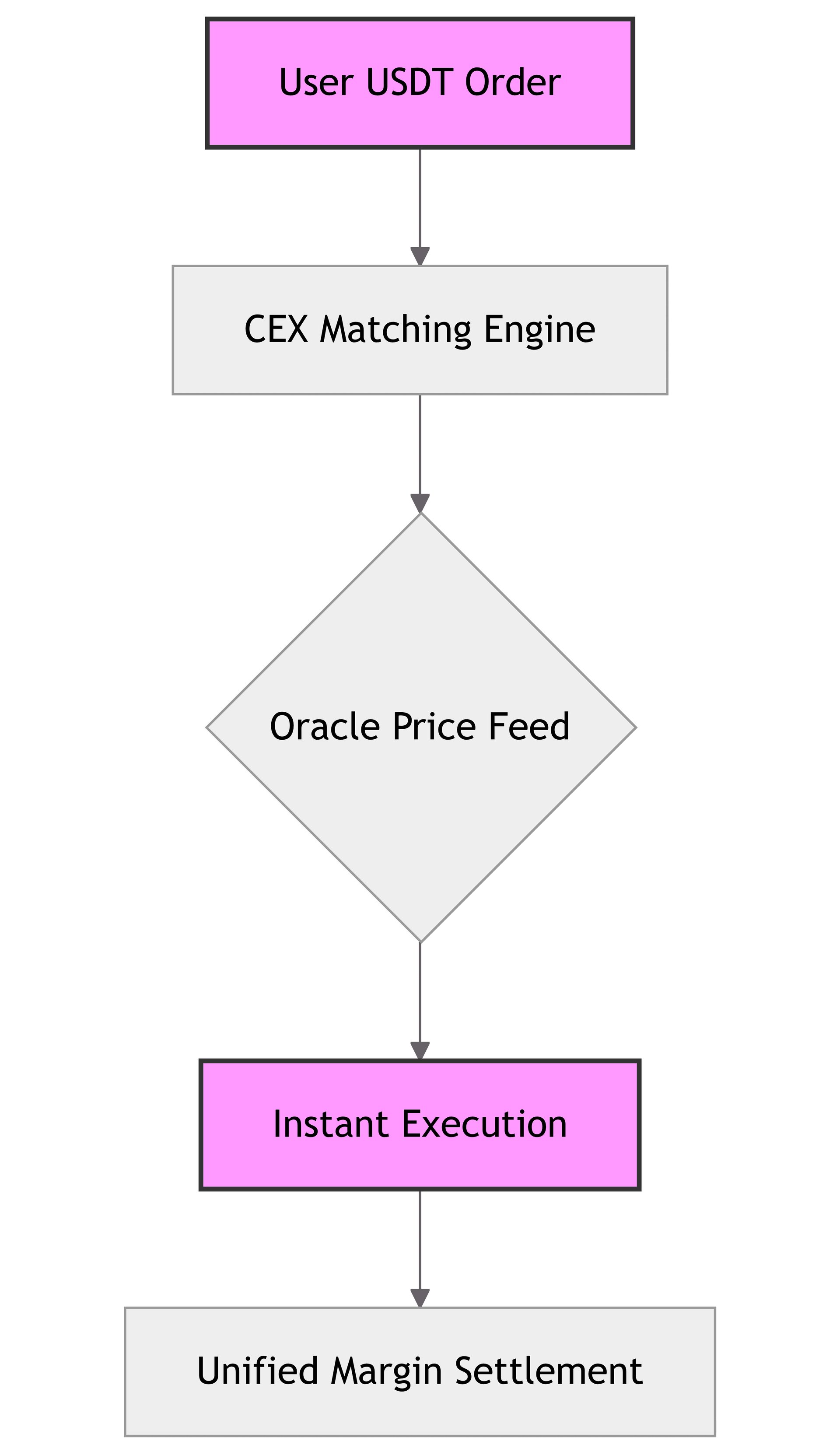

- Synthetic/Derivative Model: Positioned for price discovery and risk management. Its core lies in anchoring prices through Oracles and using cash settlement mechanisms to bypass the friction costs of physical settlement (such as T+N settlement cycles, cross-border transfer taxes, etc.). In this model, CEXs provide matching venues, greatly releasing liquidity.

Chart 1: Asset-Backed Model (Traditional Path)

Chart 2: Synthetic Asset Model (Trading Path)

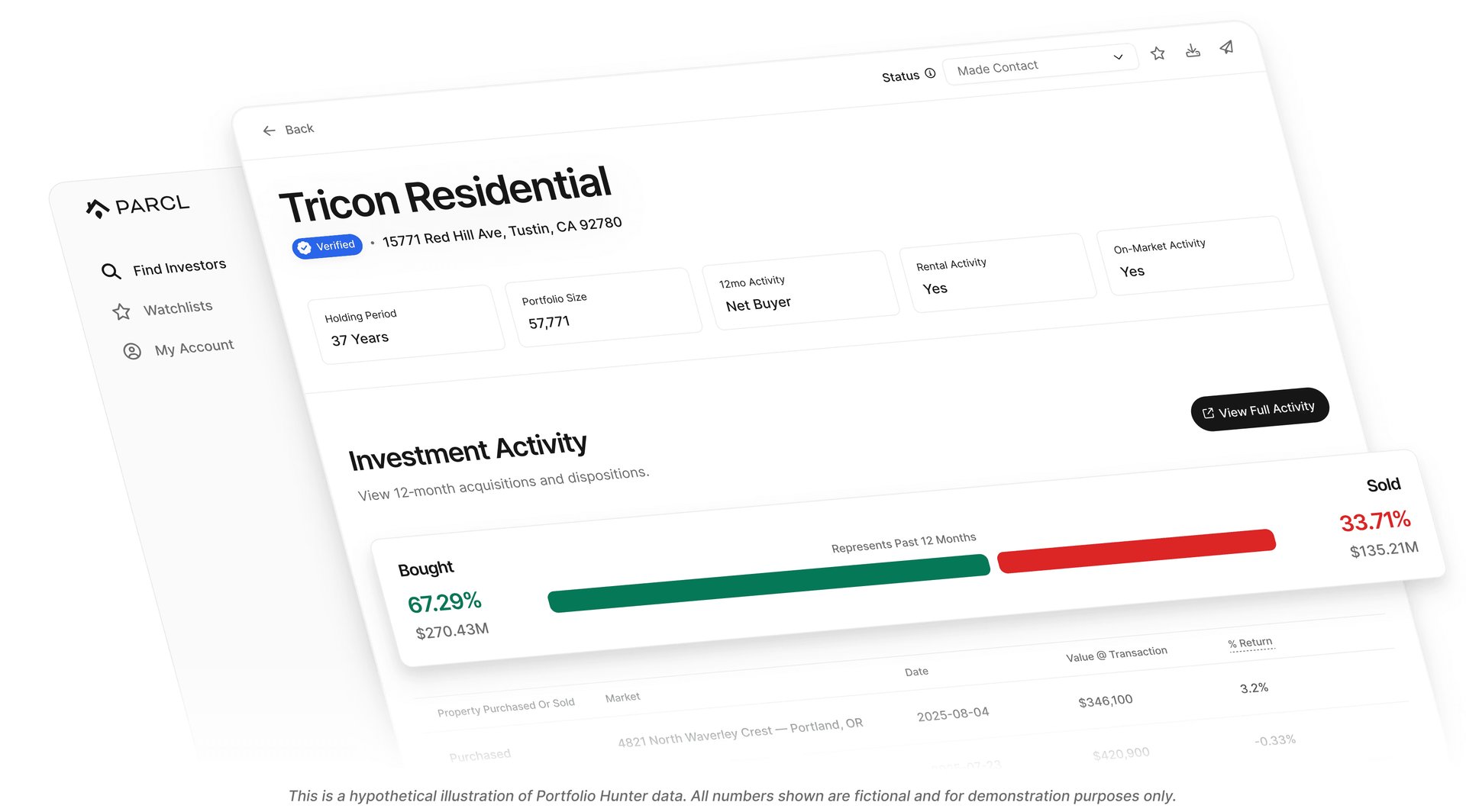

2.Deep Case Study 1: Parcl — "Abstracting Ownership" in Real Estate Trading

Parcl breaks the traditional "real estate tokenization" mindset (i.e., SPVs holding deeds and fractionalizing equity into tokens). Traditional models are constrained by the indivisibility of property and complex legal transfer processes, resulting in extremely poor secondary market liquidity. Parcl turns to building City Real Estate Indexes, allowing users to go long or short on housing price trends in specific cities (e.g., New York, Paris).

The Parcl protocol does not hold any physical property. It aggregates millions of real estate transaction data points from data providers like OASIS to generate price indexes per square foot. What users trade is "index price volatility," not property ownership.

To ensure system solvency, Parcl employs a Solvency Fund mechanism. Trading is essentially a long-short game; when longs profit, funds come from short losses. If the market becomes one-sided causing imbalance, the Liquidity Provider (LP) pool performs payouts and adjustments.

Compared to the near-zero daily turnover of physical property token projects like RealT, Parcl can reach tens of millions of dollars in daily trading volume during peak times. This fully proves the overwhelming advantage of the synthetic model of "stripping ownership, retaining risk exposure" in releasing liquidity for non-standard assets. For CEXs, integrating real estate index oracles is more scalable than establishing companies to buy buildings worldwide.

3.Release of Capital Efficiency: Unified Margin

The greatest advantage of synthetic assets lies in the ability to introduce a Unified Account system. In a CEX environment, users can use BTC, ETH, or USDT as universal collateral to directly trade risk exposures in US stocks, commodities, or real estate.

This means users do not need to sell their held crypto assets (avoiding tax events and the risk of missing out on upside) to gain returns from traditional assets or to hedge. This improvement in capital utilization is unmatched by on-chain full-collateral lending models.

III. Asset Screening: Finding Resonance Between Crypto and Tradition

Not all RWA assets are suitable for introduction into the crypto trading market. From a trading perspective, we constructed a "Three-Dimensional Assessment Model" for asset screening to measure the trading potential of traditional assets in a crypto environment:

- Volatility: Does the asset price possess sufficient trading elasticity? High volatility is a prerequisite for attracting trading capital and generating fee income.

- Relevance: Is the asset logically connected to the crypto market's macro narrative or risk logic? This determines whether users can trade (e.g., narrative resonance) or hedge (e.g., macro hedging) using familiar logic, rather than being limited to statistical positive correlation.

- Cognition: Does the asset have broad community consensus? High cognition helps lower user education costs and solves the liquidity cold-start problem.

1.Core Asset Class Analysis

Based on this assessment framework, we have screened three core asset classes that balance these dimensions.

- Equity Exposure: Mapping the AI Narrative Artificial Intelligence (AI) is the core narrative of the current tech cycle and has a natural intersection with Web3 (High Relevance). However, current AI concept tokens often lack tangible value support. Introducing synthetic trading for tech giants like NVIDIA (NVDA) not only has high cognition but can also complete investors' asset maps and solve the pain point of "users wanting to buy US stocks but facing fiat on-ramp difficulties."

- Macro Assets: Hedging and SpeculationGold and US Treasury Yields are rigid needs for macro hedging. When macro uncertainty intensifies (e.g., geopolitical wars, Federal Reserve rate cuts), crypto assets often face drastic fluctuations. Although such assets have relatively lower volatility themselves, they serve as defensive tools with extremely strong macro relevance to the crypto market.

- Proxy Assets: The Volatility Amplifier Represented by MicroStrategy (MSTR), "Bitcoin Shadow Stocks" have their own leverage attributes, giving them high volatility far exceeding BTC, making them the best carriers connecting traditional stock markets and crypto markets.

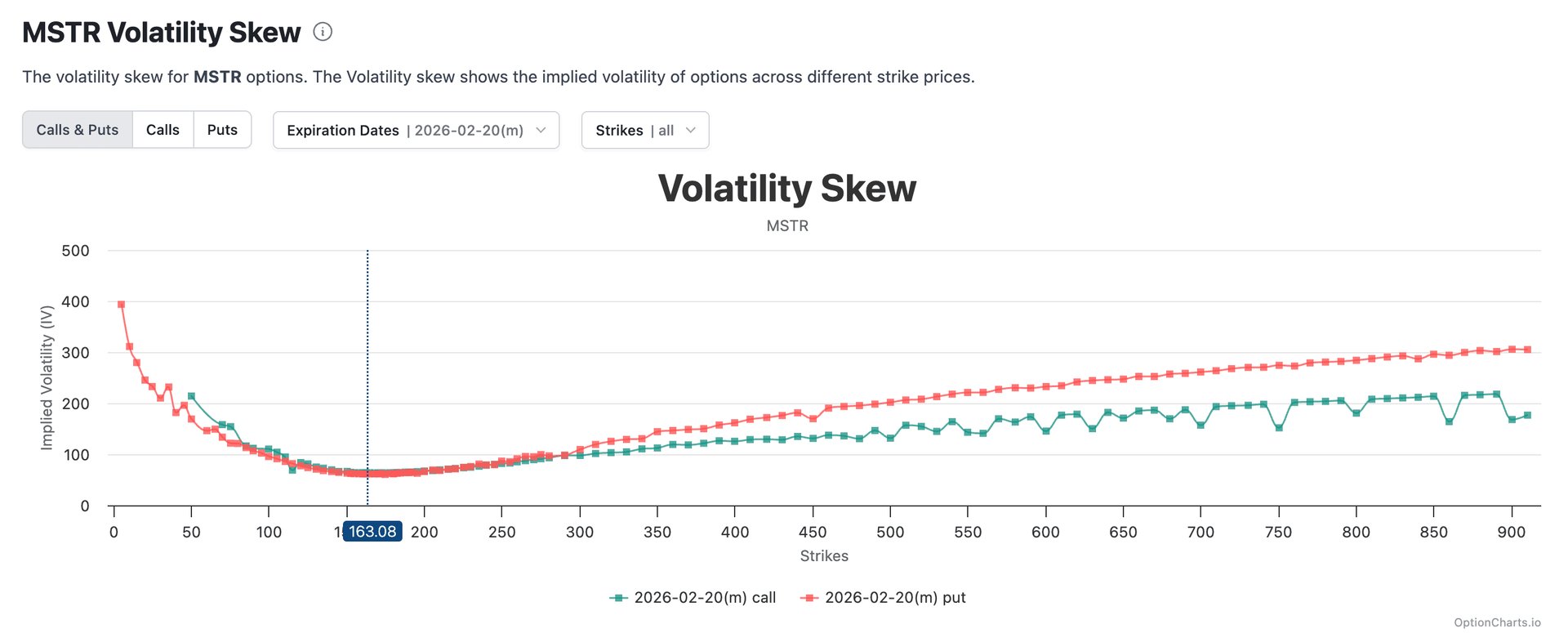

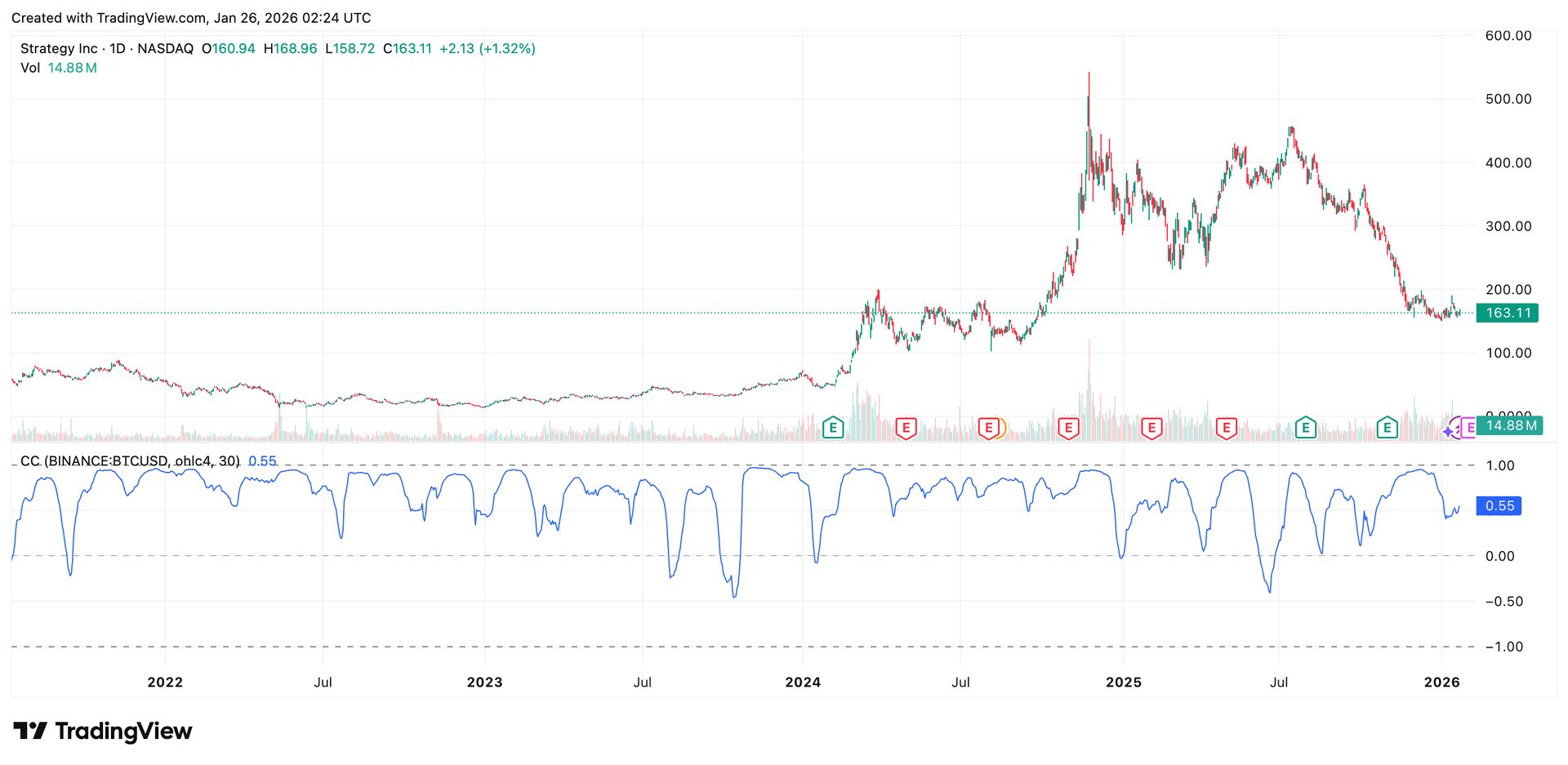

2.Deep Case Study 2: MicroStrategy (MSTR) — Volatility Premium Analysis

MSTR is essentially a holding company that purchases BTC by issuing convertible notes to add leverage. Its stock price trend is highly correlated with BTC.

According to market data, the implied volatility of MSTR options often surges to 100%-150% or even higher, while the BTC volatility during the same period typically maintains the 40%-60% range. This means MSTR's volatility is often 1.5x to 2x that of BTC, presenting a significant leverage effect premium.

The correlation between MSTR and BTC is not constant, typically fluctuating between 0.6 and 0.9. This dynamic change in correlation actually reflects the expansion and contraction of MSTR's Premium to NAV.

This high volatility characteristic offers huge opportunities for CEXs.

- For Users: Trading synthetic MSTR assets allows for capturing a more aggressive Beta return compared to directly holding BTC (with higher risk, of course).

- For Arbitrageurs: Cross-market arbitrage strategies can be constructed, such as "Long MSTR Volatility / Short BTC Volatility."

- For Exchanges: High volatility assets are a "gold mine" for fee income, with trading activity far superior to low-volatility tokenized treasuries.

IV. Deep Gaming: Options and Structured Products

1.Options: The Leap from Linear to Non-linear

Spot trading can only express linear views of "bullish" or "bearish," while options tools allow investors to trade "time" and "uncertainty." In the RWA field, the introduction of options will greatly enrich the dimension of market strategies.

For example, on the eve of a Federal Reserve meeting, investors may be unsure of the market direction but certain of high volatility. In this case, by purchasing a synthetic US Treasury yield Straddle, they can profit regardless of whether the market skyrockets or plummets.

2.Deep Case Study 3: Overtime Markets (formerly Thales) — Paradigm Shift in Prediction Markets

Overtime Markets integrated the Thales protocol, transforming from a single financial binary options platform into the largest on-chain sports and event prediction market. The key to its success lies in simplifying complex "options trading" into intuitive "event predictions" (Winner Takes All), significantly lowering the barrier for users.

Risk Control Model Advantages:

- Sports AMM (Automated Market Maker) + Peer-to-Pool: Unlike the traditional Orderbook model, Overtime uses an AMM mechanism. Users bet against a Liquidity Pool (LP) rather than finding a specific counterparty.

- Solving Cold Start: This mechanism ensures that users can obtain instant quotes and execution even in niche markets (such as macro data predictions), avoiding the liquidity dry-up problem found in orderbook models.

In the cold-start phase of RWA derivative businesses, CEXs should not be limited to professional European options but should borrow from Overtime's approach to launch "Macro Event Prediction Products" (e.g., "Will next month's CPI be higher than 3%?"). Utilizing Peer-to-Pool or Parimutuel mechanisms, exchanges can attract a large number of long-tail users through gamification and low barriers without bearing market-making risks.

3.Structured Products: Generalization of Complex Strategies

To allow more ordinary users to participate in the advanced RWA trading market, packaging complex option strategies into structured wealth management products will be a potential product trend.

Product Concept: "Fixed Income+" RWA Wealth Management

- Underlying Asset: 80%-90% of funds purchase on-chain treasuries (belonging to the Fundamental Asset Layer) to ensure principal safety and generate base interest.

- Enhanced Yield: Interest generated from treasuries is used to purchase call options linked to Gold or Tech Stocks (belonging to the Financial Trading Layer).

- Advantage: This type of product retains the stability of fundamental assets while incorporating the high-yield potential of synthetic assets, making it easily acceptable to mass investors.

V. The Role of Trading Venues: CEX as the "Super Connector"

1.Solving Liquidity Fragmentation & Aggregation Advantage

Although on-chain DEXs have advantages in transparency, they still face challenges with oracle latency and gas fee friction when handling high-frequency trading of RWA derivatives. CEXs, through centralized high-performance matching engines, can aggregate liquidity across multiple asset classes, providing order book depth and slippage experience superior to on-chain AMMs.

Furthermore, utilizing synthetic asset characteristics, CEXs can break the time and space constraints of traditional financial markets, offering 24/7 trading services. For example, during US stock market closures, users can still react to breaking news on CEXs via pre-market and after-hours data feeds.

2.The Hub of Credit and Risk Control

In synthetic asset trading, the exchange essentially plays the role of a Central Counterparty (CCP).

- Risk Isolation: CEXs can effectively isolate the extreme volatility risks of synthetic assets from the crypto-to-crypto trading sectors by establishing independent Insurance Funds and Auto-Deleveraging (ADL) mechanisms.

- Compliance Buffer: In jurisdictions like Singapore and Hong Kong, Contract for Difference (CFD) businesses based on indexes have clearer and more mature regulatory frameworks than direct Security Token Offering (STO) issuance, providing possibilities for rapid business deployment.

VI. Conclusion and Outlook

2026 will be a turning point for the RWA market. We predict the market will present a "dual-track" trend: on-chain protocols will continue to solidify the infrastructure for asset issuance and ownership confirmation, while exchanges will dominate the restructuring of asset liquidity and the extension of trading scenarios.

By introducing synthetic assets and options strategies, we are building a "Boundary-less Trading Layer." In the near future, investors will be able to seamlessly trade Tokyo's Yen exchange rate, New York's tech stock options, and on-chain DeFi yields within a single account using Bitcoin as margin. This is not only the ultimate release of capital efficiency but also the ultimate vision of the new digital finance infrastructure.

References

- Parcl Protocol Documentation: https://docs.parcl.co/

- MicroStrategy Investor Relations: https://www.microstrategy.com/en/investor-relations

- Overtime Documentation: https://docs.overtime.io/

- J.P. Morgan: https://www.jpmorgan.com/content/dam/jpm/cib/complex/content/securities-services/regulatory-solutions/evolution-of-digital-assets.pdf

- Ostium Documentation: https://ostium-labs.gitbook.io/ostium-docs

Disclaimer

This report is prepared by Bifu Research Institute and is for information purposes only. It does not constitute any investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance does not indicate future returns. Users should fully assess risks and consult professional advisors before investing.

The policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may be updated and adjusted over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.