From Accounts to Tokens: The Battle of Payment Infrastructure between SWIFT and Stablecoins

25/02/202606:22:32

Bifu Research | 2026

Abstract

In 2026, the global cross-border payment market is at a critical juncture of generational infrastructure replacement. The account-based interbank network, long dominated by SWIFT, is facing strong challenges and penetration from token-based networks represented by stablecoins.

The market landscape is no longer a single-dimensional competition. With the full implementation of gpi (Global Payment Innovation) and ISO 20022 standards, SWIFT has successfully fortified its moat in the high-value clearing sector with stringent compliance requirements. Meanwhile, stablecoins are no longer limited to crypto-asset trading but have achieved asymmetric strikes in retail payments, high-frequency trading, and emerging market remittances through their 24/7 operation and atomic settlement capabilities.

Bifu Research believes that with breakthroughs in "controlled reversibility" of blockchain technology—introducing error-correction mechanisms at the compliance level while maintaining ledger immutability—the risk management barriers for institutional adoption of tokenized payments have significantly decreased. Coupled with the rigid demand of the global digital economy for instant liquidity and 24/7 settlement, the global payment system is evolving from a single-track bank network into a dual-track complementary new paradigm where "SWIFT holds the wholesale end, and stablecoins reshape the retail end."

I. Macro Background: The "Impossible Trinity" of Cross-Border Payments

For a long time, the cross-border payment industry has been trapped in the "Impossible Trinity" where speed, cost, and compliance transparency are difficult to achieve simultaneously. Traditional financial institutions must balance liquidity costs with Anti-Money Laundering (AML) compliance requirements in complex correspondent banking networks, leading to a terminal user experience that is often expensive and sluggish. To understand the root of this dilemma, it is necessary to distinguish between two fundamentally different value transmission systems.

1.Limitations of the Account-Based System

Systems represented by SWIFT and traditional banks are "account-based." In this model, funds do not move physically; instead, they rely on a series of debit and credit record updates in bilateral ledgers. To complete a cross-border payment, the information flow (SWIFT messages) and the fund flow (clearing system) are often separated, leading to tedious reconciliation processes and heavy reliance on the credit endorsement of intermediaries.

2.Disruptiveness of the Token-Based System

Systems represented by stablecoins are "token-based." Tokens are not just carriers of information but the value itself. In a blockchain network, a transfer is a physical (digital) transfer of value, without the need for intermediary reconciliation. This "transaction as settlement" characteristic fundamentally eliminates the intermediary costs of multi-layered correspondent banks.

By 2026, market data has fully verified the rise of the token system. The annual transaction volumes of USDC and USDT have reached levels comparable to major card networks (such as Visa), proving that stablecoins are no longer marginal innovations but systemically important financial infrastructure.

II. Defense of the Traditional Hegemon: SWIFT's Digital Counterattack

Faced with the challenge of fintech, SWIFT has not stood still but has launched a profound digital self-innovation. This counterattack is mainly reflected in two dimensions: efficiency improvements through gpi and data restructuring through ISO 20022.

1.SWIFT gpi (Global Payment Innovation): From Black Box to Transparent Logistics

Traditional cross-border payments were like sending a standard letter; the status remained unknown once sent. gpi introduced a unique end-to-end transaction reference (UETR), similar to a courier tracking number. This number accompanies the message through the entire correspondent banking chain, and all participating banks must upload processing status in real-time to a cloud-based Tracker database.

This mechanism enables visualization of payment status. More importantly, gpi enforces stricter interbank Service Level Agreements (SLAs), requiring banks to complete processing within a specified timeframe. Data shows that approximately 75% of gpi cross-border payments now reach the beneficiary bank within 10 minutes, completely shattering the stereotype of SWIFT being "inefficient and slow."

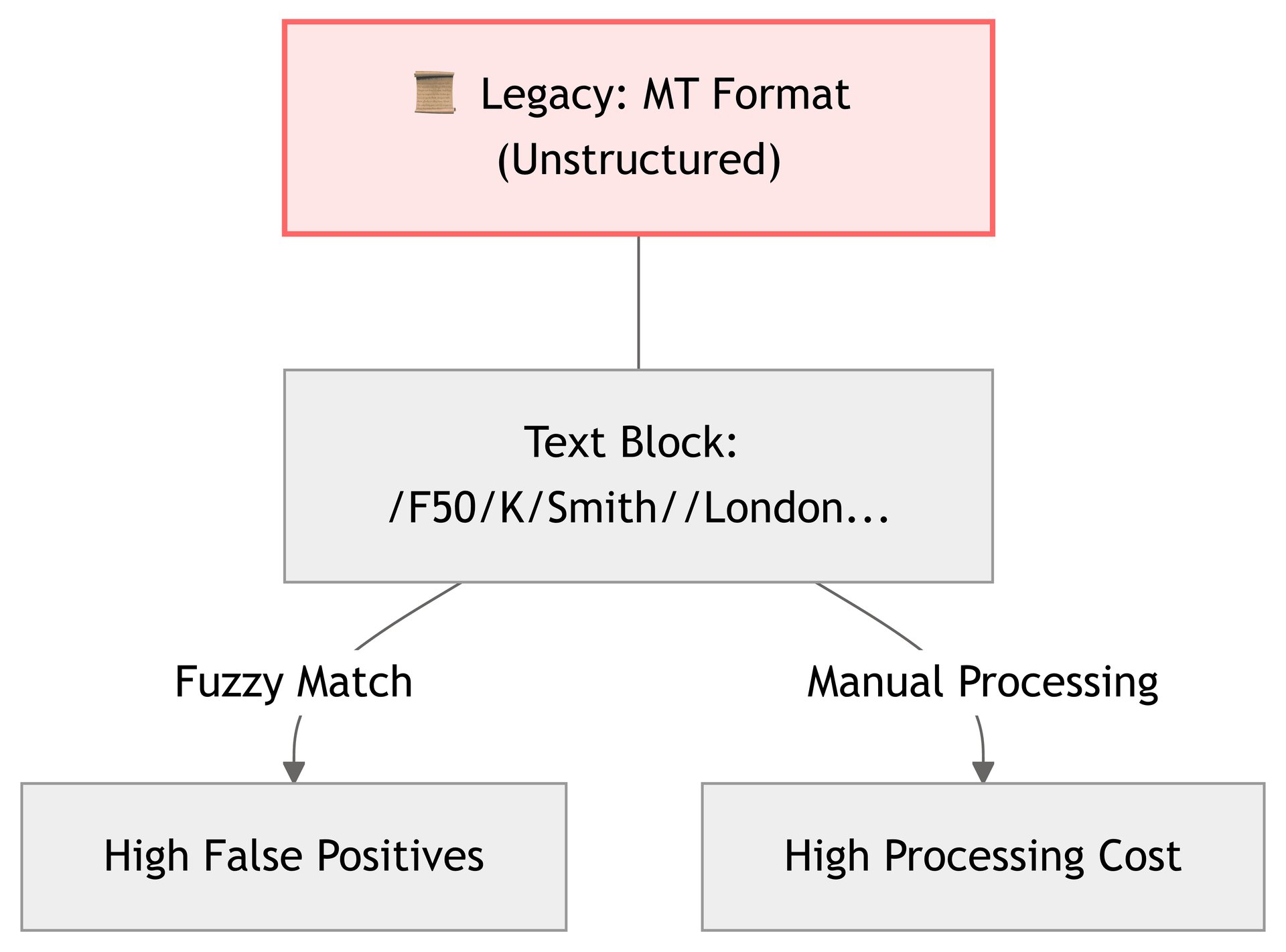

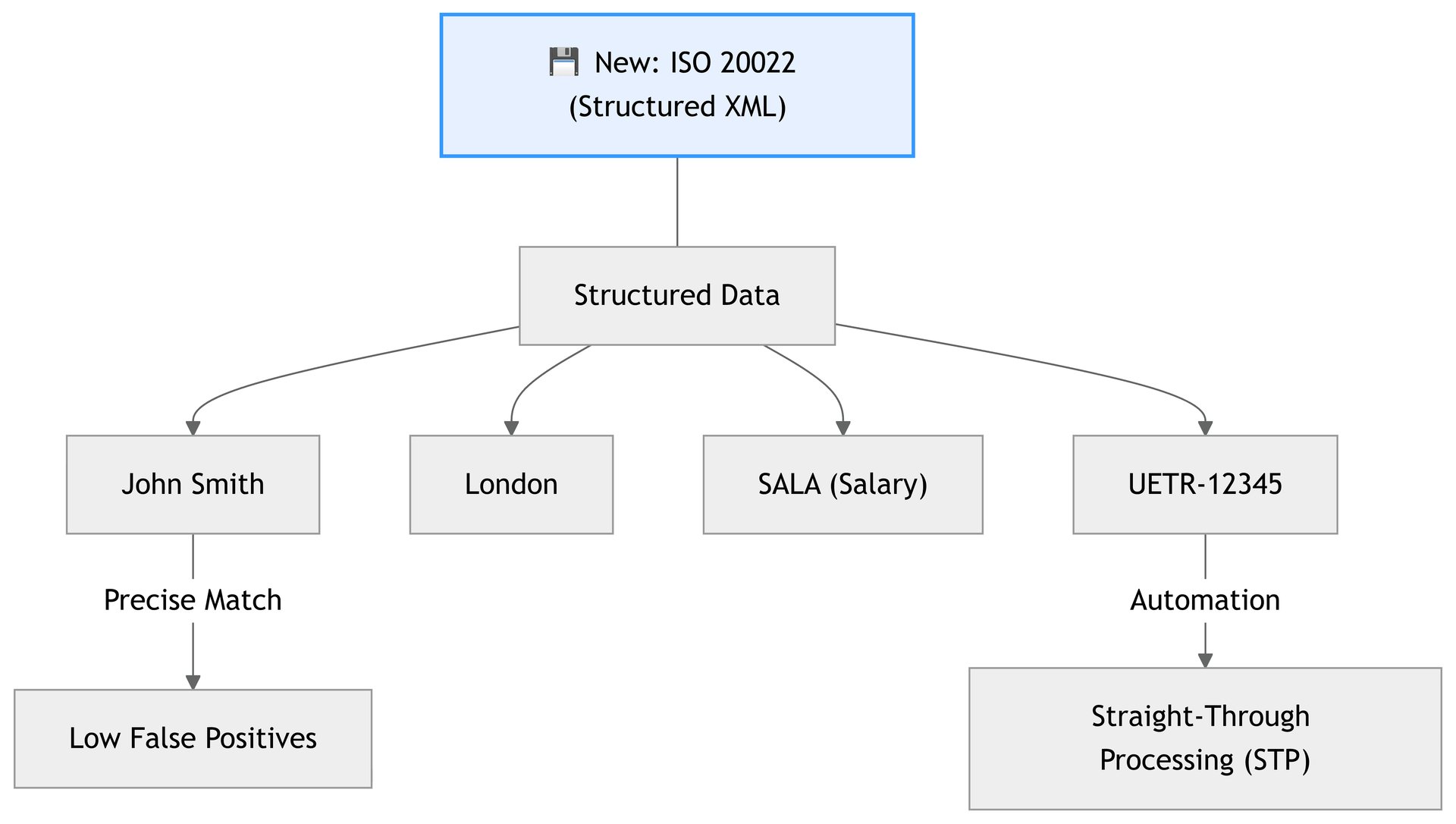

2.ISO 20022 Migration: From Text to Structured Data

This is a complete migration from the legacy MT format (unstructured text) to the MX format (XML-based structured data). The old format had limited character counts and vague information, whereas ISO 20022 provides rich and standardized data fields that can accommodate detailed remitter addresses, ultimate beneficiary information, and complex remittance purpose codes.

Core Value:

- Improved Straight-Through Processing (STP) Rate: Structured data eliminates the need for manual intervention, allowing machines to read and process messages directly, reducing returns caused by formatting errors.

- Enhanced Compliance Screening: In AML screening, precise data fields allow systems to accurately distinguish between "entities with the same name," significantly reducing false positives and solving the pain point of payment delays caused by compliance blocks.

Furthermore, regarding retail payments, new regulations launched by SWIFT in 2026 further leverage the above technical foundations to mandate price transparency and eliminate hidden fees, attempting to fix shortcomings in user experience.

3.Challenge: The Time Lag of "Turning the Elephant"

Although these technical upgrades are in the right direction, execution efficiency is hindered by "coordination costs." For instance, ISO 20022 took nearly ten years from project initiation in 2016 to full mandatory execution in 2025. This is because SWIFT connects over 11,000 institutions worldwide, and its upgrade speed is limited by the weakest participating parties (the bottleneck effect). Additionally, the core banking systems of traditional banks are often based on mainframe architectures from decades ago; modifying data structures implies a fundamental and painful system overhaul. This long iteration cycle makes SWIFT appear inadequate in responding to consumer demand changes compared to Fintech competitors who can complete a protocol upgrade in months.

III. Core Comparison: Technical Architecture and Business Logic

This chapter delves into the underlying technology to analyze why modern financial business urgently needs new infrastructure even as SWIFT has significantly accelerated.

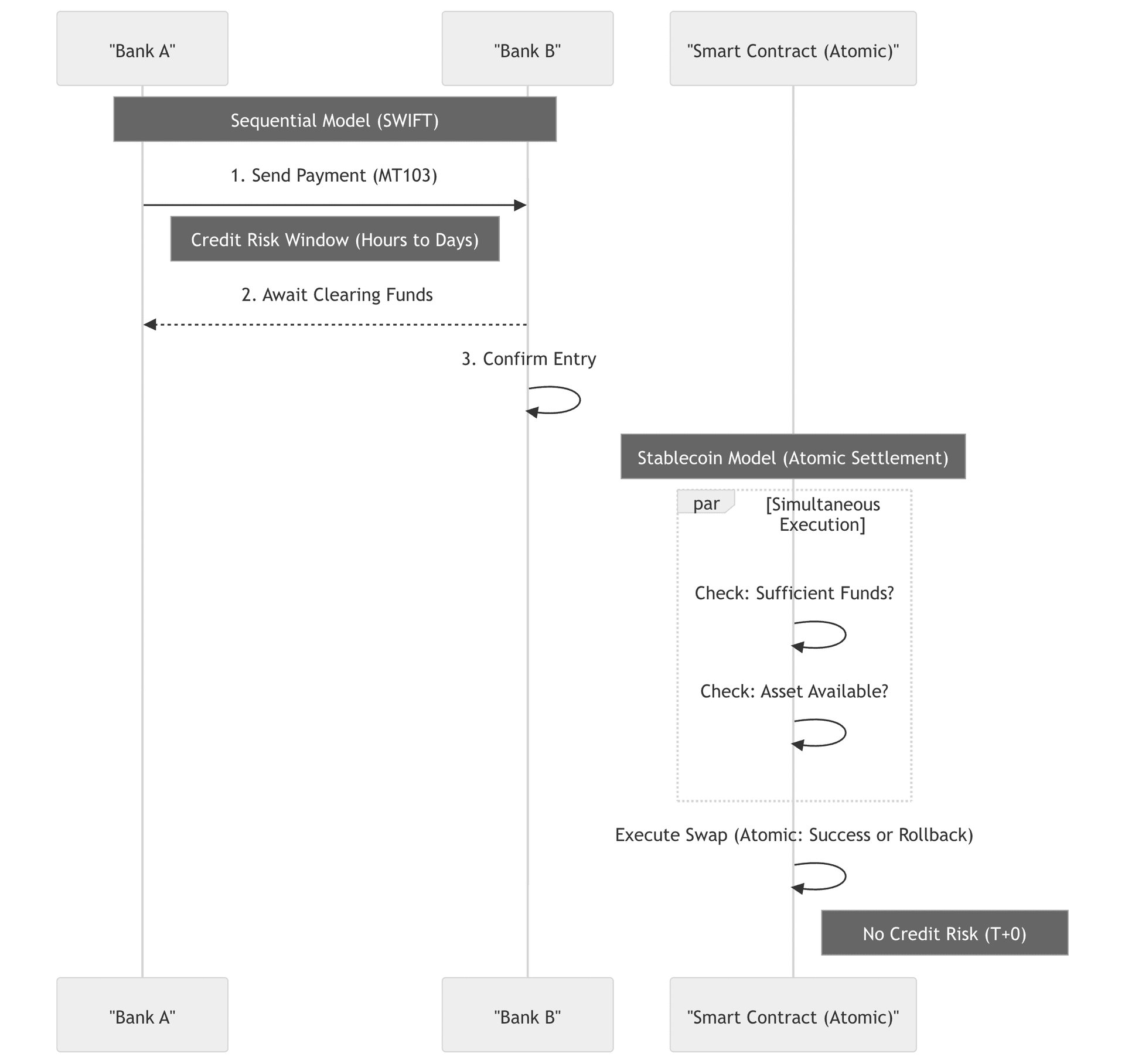

1.Settlement Mechanism: Sequential Processing vs. Atomic Exchange

The SWIFT system employs a sequential "separation of communication and fund flow" model. Bank A sends a payment message to Bank B, and Bank B updates its ledger upon receipt. During this process, if one party fails before the actual fund transfer, credit risk (Herstatt Risk) arises. In contrast, stablecoin systems use "Atomic Settlement." The transfer of funds and the delivery of assets are completed simultaneously within the same smart contract transaction—either both succeed or both fail. This mechanism fundamentally eliminates counterparty risk, making "delivery versus payment" possible, which is crucial for large-scale asset transactions.

2.Capital Efficiency: T+N vs. T+0

In the traditional correspondent banking model, to ensure smooth payments, banks must pre-position large amounts of idle funds in correspondent accounts (Nostro Accounts) worldwide. This not only traps valuable liquidity but also brings huge opportunity costs. Stablecoin networks break this deadlock through a 24x7x365 operation mechanism. They release liquidity locked by weekends, holidays, and bank closing times, allowing capital turnover rates to reach theoretical limits. For multinational corporations, this means they can maintain the same business operations with less cash flow.

3.Breaking Key Challenges: How to achieve "Recovery" on an "Immutable" Ledger?

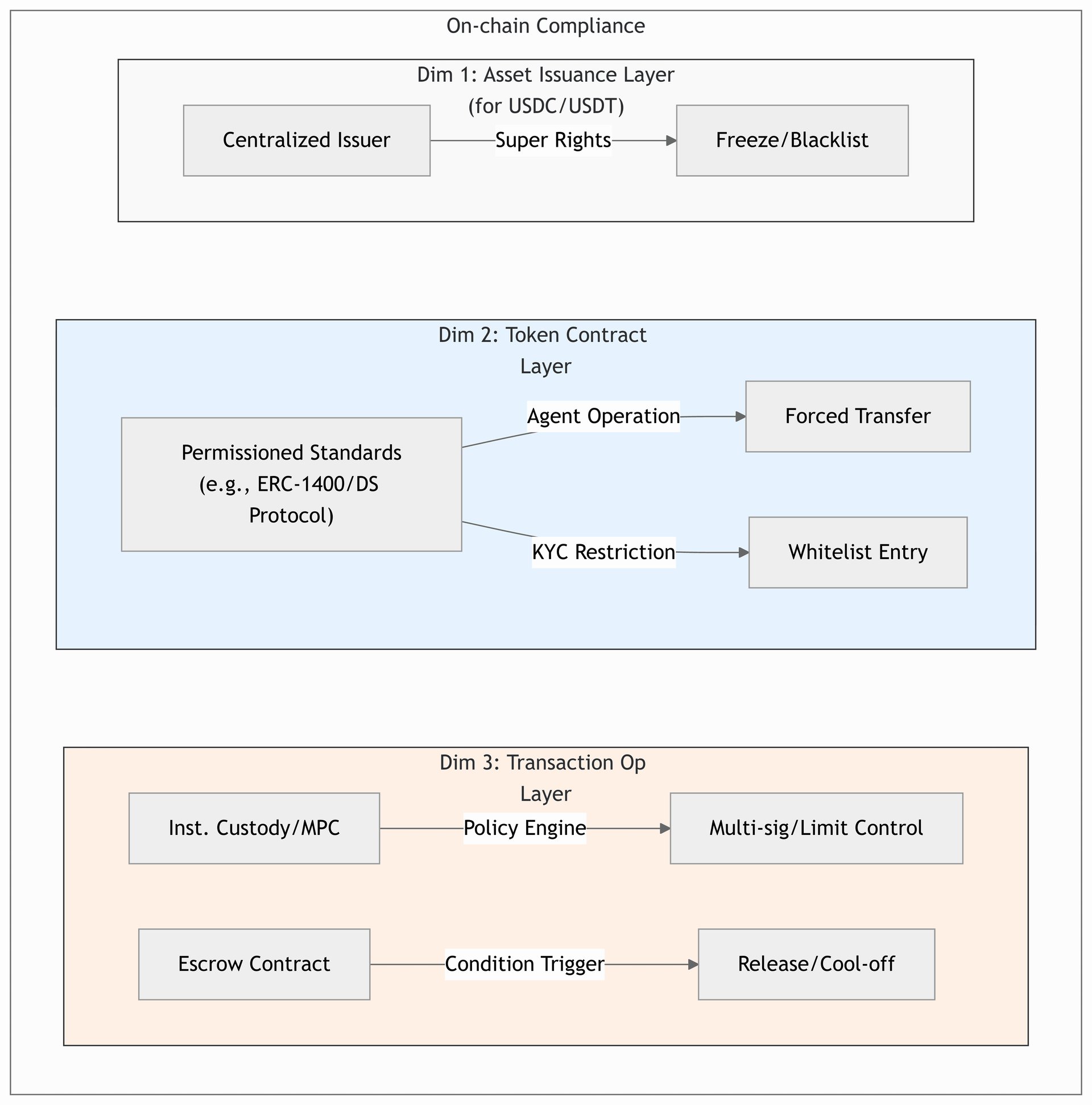

The native "immutability" of blockchain was once the biggest obstacle for institutional adoption. In traditional finance, errors can be rolled back through bank service tickets, but on a blockchain, once a private key signs, the asset is irreversible. To resolve this fundamental conflict between compliance and risk control, the industry has evolved multi-layered "controlled reversibility" solutions:

3.1Dimension 1: Centralized Issuer Intervention

For fiat-backed stablecoins like USDC and USDT, issuers retain "super-user permissions" at the contract level. In case of hacks or requests from law enforcement, Circle or Tether can directly freeze assets in involved addresses or even burn and remint them. While this method has lower efficiency and relies on manual labor, it provides a basic safety net.

This mechanism has been widely applied. Circle (USDC issuer) and Tether have repeatedly cooperated with law enforcement to freeze funds in addresses suspected of money laundering or theft, which has become a standard practice for compliant stablecoin operations.

3.2Dimension 2: Permissioned Token Standards (for RWA/Institutional Tokens)

For complex institutional financial business, the industry has developed various permissioned token standards, such as ERC-3643, ERC-1400, and Securitize's DS Protocol. While technical details vary, the core logic is consistent: embedding a "governance layer" within the token contract.

First, these standards implement pre-emptive risk blocking through built-in whitelist mechanisms, ensuring only KYC-verified addresses can interact, effectively preventing funds from flowing into sanctioned entities. Second, to solve the "irreversibility" of on-chain assets, the standards introduce "Forced Transfer" functions. Through a preset Agent role, in the event of private key loss, court enforcement, or serious errors, the agent has the right to compliantly transfer assets to a secure address without the original holder's private key signature, granting on-chain assets the same legal enforceability as traditional financial assets.

BlackRock's BUIDL fund is a typical case. The fund implements strict investor whitelist management and asset freezing functions through Securitize's proprietary protocol, thereby meeting the regulatory requirements of the U.S. Securities and Exchange Commission (SEC).

3.3Dimension 3: Escrow Smart Contracts

In transaction workflows, institutions are increasingly adopting programmable Escrow contracts. Funds are no longer transferred directly peer-to-peer but first enter an escrow contract for locking. Funds are released only after specific conditions are met (e.g., oracle verification, cooling-off period end, or multi-sig confirmation). This "code-level intermediary" provides a safety buffer similar to guaranteed transactions while retaining decentralized efficiency.

In the payment sector, institutional-grade custodians like Fireblocks have built approval flows based on Policy Engines, essentially acting as off-chain "pre-escrow"; while PayPal, in its PYUSD payment flow, also achieves similar transaction protection through the coordination of a centralized ledger and on-chain settlement.

4.Iteration Speed: Institutional Coordination vs. Machine Consensus

For SWIFT, the core challenge lies in an iteration mechanism based on "human" institutional coordination. Any underlying protocol upgrade (like ISO 20022) requires tens of thousands of financial institutions worldwide to synchronize system updates. This involves not only massive technical costs but also lengthy cross-border and cross-institutional negotiations, resulting in a system evolution process that is extremely slow and expensive, often planned in decade-long units.

In contrast, stablecoin networks rely on machine consensus. Protocol upgrades (such as migrating from ERC-20 to more efficient standards) are typically completed through code forks or proxy contract upgrades, requiring only technical consensus among network validation nodes. This "code as law" characteristic grants stablecoin networks exponential innovation speed, allowing them to quickly respond to market demands and perform seamless iterations, thereby gaining an agility advantage in competition with traditional systems.

IV. Catalysts: Capital Efficiency and the Push of the 24/7 Economy

If the improvement of payment efficiency is "the icing on the cake," then the pursuit of extreme capital efficiency is "providing charcoal in the snow." The global financial market is evolving from "daily settlement" to "real-time settlement," becoming the strongest catalyst for the popularization of new payment systems.

1.Capital Drag of the Traditional T+N Model

In existing banking systems, cross-border funds often take T+2 or even longer to finally confirm. This forces multinational corporations and financial institutions to hold large redundant liquidity buffers to cope with the uncertainty of settlement cycles. In a fluctuating interest rate environment, the idle cost of this capital is immense.

2.Immediate Demand of the 24/7 Economy

The digital economy runs 24/7, but traditional banking systems follow a "9-to-5" workday logic. This mismatch leads to liquidity gaps for e-commerce platforms, streaming services, and global trade during weekends and holidays. Enterprises urgently need a fund carrier that can flow in real-time like information and never sleeps.

3.The Rise of Programmable Finance

Beyond speed, modern finance demands "intelligence." Whether it's automated supply chain revenue sharing, condition-triggered option settlement, or instant settlement of RWA (Real World Assets), all require funds to be programmable. Only T+0 and programmable funds (stablecoins) can match T+0 and intelligent business logic. This logic of the business layer forcing upgrades at the fund layer is driving "On-chain DvP" (Delivery versus Payment) and "Streaming Payments" as new industry standards.

V. Conclusion and Outlook: Towards Infrastructure Integration and Dual-Track Parallelism

The global cross-border payment system is undergoing a paradigm shift from "information transmission" to "value transmission." Looking ahead, this system will not move toward uniformity but will exhibit deep infrastructure integration and a clear layered landscape.

1.Future Landscape

Giants like Stripe, Visa, and Mastercard have already begun using stablecoins as their backend clearing rails. For terminal users, the payment experience remains the familiar bank app or card swipe, but in the invisible backend, funds are cleared at lightning speed through blockchain networks in the form of stablecoins. The payment map will show clear layers:

- Top Layer (Sovereign and High-Value): SWIFT and RTGS (Real-Time Gross Settlement) systems will continue to dominate ultra-large-value, confidential, government-to-government, and interbank position transfers; their compliance and certainty are irreplaceable.

- Middle Layer (Institutional and Commercial): Compliant stablecoins (such as USDC, PYUSD) will dominate corporate cross-border trade settlement, supply chain finance, and various digital asset transactions, becoming the preferred tool for interbank liquidity management.

- Bottom Layer (Retail and Long-tail): In emerging markets, cross-border e-commerce, and the gig economy, stablecoins (and some offshore stablecoins) will fill the gaps in traditional banking services with low costs and high accessibility.

2.Strategic Implications

From a regulatory perspective, focus is undergoing a profound shift. Simple "crypto prohibition" strategies are inadequate for the globalized digital economy. The core challenge ahead lies in how to regulate the governance of programmable money, particularly establishing a cross-jurisdictional legal framework for on-chain asset disposal. This means regulators must adapt to a new hybrid reality: technical logic ("code as law") will coexist with existing national laws for the long term. Establishing effective links and balances between the two will be the key to future legislation.

From an institutional perspective, the binary choice between clinging to tradition or going completely radical is no longer applicable. In the next five years, the core competitiveness of financial institutions will depend on whether they can build efficient "hybrid middleware"—a technical architecture capable of handling both standardized SWIFT messages and seamless interaction with on-chain smart contracts. Only by actively embracing this dual-track hybrid reality can traditional institutions reshape their irreplaceability and remain invincible in this profound payment revolution.

Disclaimer

This report is prepared by Bifu Research Institute and is for information purposes only. It does not constitute any investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance does not indicate future returns. Users should fully assess risks and consult professional advisors before investing.

The policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may be updated and adjusted over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.