US Digital Finance Compliance Landscape: On-Chain Reshaping of the Dollar System and New Asset Regulations

16/01/202603:30:07

BifuResearch | 2026

Executive Summary

The United States is leading a profound paradigm shift from "Cryptocurrency" to "Compliant Digital Finance." Its core strategy is neither a simple ban nor laissez-faire, but rather precise legislative measures—exemplified by the GENIUS Act—that clearly bisect the complex digital asset market into two distinct sectors: "Payment Tokens" as settlement tools and "Investment Tokens" as value carriers.

This report aims to analyze the far-reaching impact of this transformation on the global market through the lens of US top-level regulatory design. We believe that under the new compliance order, RWA (Real World Assets) is no longer just a niche sector, but the inevitable form of "Investment Digital Assets" within a compliant framework. As a global digital asset service provider, Bifu is committed to standing at the forefront of the industry, cutting through the regulatory fog to identify opportunities for users and introduce the most secure, high-quality assets.

I. Macro Trends: The "Dollarization" Process of Digital Assets

1.Market Landscape: Absolute Dominance of Dollar-Denominated Assets

In past crypto market cycles, although Bitcoin (BTC) and Ethereum (ETH) occupied the market cap high ground, examining the "unit of account" and "medium of settlement" reveals that the market has effectively completed a silent "dollarization" movement.

According to data monitoring by Bifu Research:

- Stablecoin Market: Over 90% of trading volume is carried by US dollar-pegged stablecoins (such as USDT, USDC).

- RWA Assets: More than 90% of underlying assets in top RWA projects (including tokenized treasuries and private credit) are dollar-denominated assets.

This data indicates that the digital asset market does not exist independently of the traditional financial system but has instead become a new extension of dollar liquidity. The strategic intent of US regulators is not to stifle innovation, but to ensure that the underlying unit of account for the on-chain financial system remains the US dollar through a rigorous compliance framework, thereby extending its monetary dominance in the digital economy era.

2.Institutional Cornerstone: The GENIUS Act and the Legalization of the Digital Dollar

The GENIUS Act (Guiding and Establishing National Innovation for US Stablecoins Act), effective in 2025, is the concentrated embodiment of this strategic intent. It is not merely a stablecoin management bill, but an "infrastructure bill" for the US digital financial system.

- Establishing Legal Status: The act grants non-bank issuers (such as Circle, Paxos) the right to operate legally under the supervision of the OCC (Office of the Comptroller of the Currency), breaking the monopoly of traditional banks on currency issuance.

- Eliminating Systemic Risk: By mandating a 1:1 reserve of cash or short-term treasury bills, the act eliminates the biggest "black box" risk in digital asset trading—the opacity of settlement tools.

For the industry, although the GENIUS Act is stringent, it formally establishes the role of the "private digital dollar" as the on-chain trade settlement currency, laying a solid legal foundation for more complex financial activities above it.

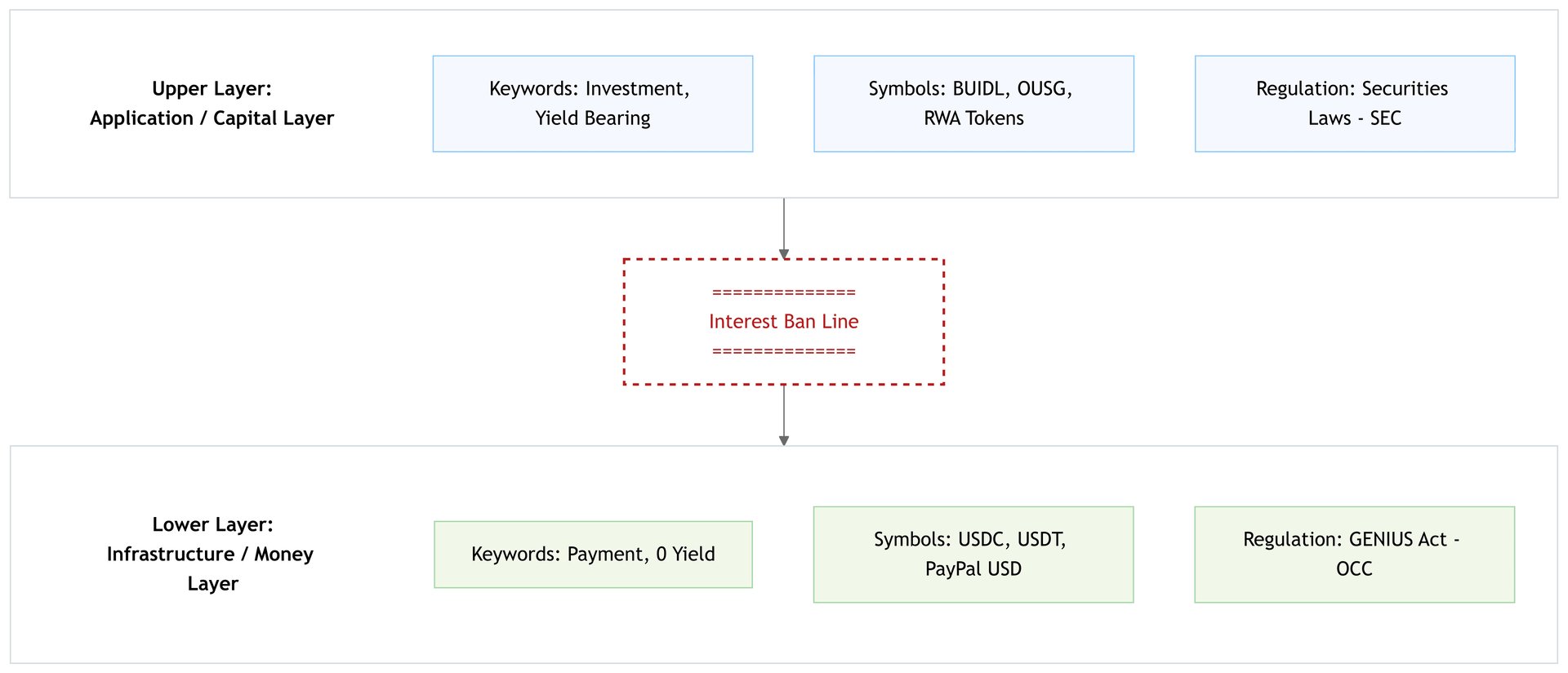

II. Functional Divergence: The "Great Divide" Between Payment and Investment

1.Interest Ban and Asset Attribute Reshaping

The key to understanding US regulatory logic lies in recognizing an insurmountable red line drawn by the GENIUS Act: Payment stablecoins must not pay interest.

This clause aims to strictly distinguish between "monetary functions" and "investment functions," preventing non-bank payment institutions from evolving into unregulated shadow banks. Consequently, the digital asset market is forcibly restructured into two parallel worlds:

- Money Layer: Represented by USDC/USDT

- Attributes: Emphasizes high liquidity, price stability (1.00 USD), and payment properties.

- Yield: Zero yield. Holding it is for trade settlement or store of value, not for appreciation.

- Regulator: Primarily under the jurisdiction of the OCC or state banking regulators.

- Capital Layer: Represented by Tokenized Treasuries (RWA)

- Attributes: Emphasizes value carriage and yield distribution.

- Yield: Has yield (e.g., US Treasury yields).

- Regulator: Redefined as "securities," strictly under the jurisdiction of the SEC (Securities and Exchange Commission).

2.Limitations of Bank-Issued Deposit Tokens

In this context, bank-issued "deposit tokens" (such as JPM Coin), once held in high regard, face an awkward situation. Due to constraints from traditional bank balance sheet regulations and technological barriers to interbank settlement, deposit tokens are largely confined to B2B wholesale settlement between institutions and struggle to reach ordinary crypto users. Objectively, this leaves a massive retail-grade investment asset market vacuum—which is precisely where the opportunity for RWA rises.

III. Compliance Breakout of Investment Assets: RWA as a Case Study

1.The Universal Dilemma Under the Howey Test

In the US, the SEC Chair has repeatedly emphasized: "The vast majority of crypto tokens are securities." According to the Howey Test, as long as four elements—"investment of money, in a common enterprise, with a reasonable expectation of profits, to be derived from the efforts of others"—are involved, it is deemed a security. This leaves a Sword of Damocles hanging over numerous DeFi projects and ICO tokens promising yields.

In contrast, RWA (especially tokenized US Treasuries) has charted a different path: it does not attempt to evade the "security" definition but actively embraces regulation, becoming the only exemplar of "Investment Digital Assets" capable of navigating the institutional compliance path currently.

2.Path A: Chartered Runway (Traditional Finance Giant Model)

Represented by BlackRock (BUIDL) and Franklin Templeton (Benji).

- Model: Strictly adheres to US securities laws (e.g., Reg D or 1940 Act registration).

- Features: Extremely high compliance, issuing fund shares directly on-chain.

- Limitations: Serves only Qualified Institutional Buyers (QIBs) and has high investment thresholds. This creates a natural barrier between them and the vast Web3 retail market, despite their massive volume.

3.Path B: Offshore Architecture (Crypto-Native Model)

Represented by Ondo Finance and Tether Gold.

- Model: "Underlying Assets in the US + Issuance and Sales Abroad." An SPV (Special Purpose Vehicle) holds US ETFs or Treasuries, but tokens are issued in non-US jurisdictions, utilizing Reg S exemptions to block US investors.

- Implication: This model successfully introduces yields from high-quality US assets to the global crypto market. It satisfies asset-side compliance requirements while retaining the liquidity and accessibility needed by the DeFi world. This is currently the most effective bridge connecting the Web3 ecosystem.

IV. Infrastructure Upheaval: The Repeal of SAB 121 and the New Era of Custody

1.Historical Turning Point: The End of SAB 121

For a long time, the SEC's SAB 121 (Staff Accounting Bulletin No. 121) was the biggest stumbling block preventing traditional banks from entering the digital asset custody market. It required custodians to record user crypto assets on their balance sheets and set aside expensive capital reserves, effectively "dissuading" all major banks economically.

With the formal repeal of this bulletin in 2025, an invisible financial Berlin Wall has been toppled.

2.The Return of Bank-grade Custody

The repeal of SAB 121 rapidly changed the market landscape:

- Giants Entering the Arena: Global custodial banking giants (such as BNY Mellon, State Street) are no longer restricted and have begun providing custody services for Bitcoin and tokenized assets (RWA) to institutional clients on a large scale.

- Reputation Premium: For traditional large funds like pensions and insurance funds, "private keys held by BNY Mellon" carries a natural compliance persuasiveness compared to "private keys held by a tech startup."

3.Profound Impact on RWA

This infrastructure upgrade is revolutionary. It means the security of RWA assets can finally reach "Bank-grade" standards. For RWA project teams, accessing traditional bank custody not only lowers the risk of hacker attacks but also serves as a "Gold Standard" for gaining the trust of institutional investors.

V. Market Outlook and Bifu's Global Asset Perspective

1.Exchange Strategy: Building a Comprehensive Compliant Ecosystem

Based on in-depth analysis of US regulatory trends, Bifu believes that future digital asset trading platforms should not be limited to a single "speculation" logic but should build a compliant asset ecosystem covering the full lifecycle.

- Money Layer - Embracing the "Compliance Cornerstone": For payment tokens, Bifu actively embraces compliant stablecoins protected by the GENIUS Act. We will continue to introduce and maintain deep, compliant US dollar stablecoin trading pairs, ensuring the absolute safety and liquidity of user assets in a "resting state."

- Capital Layer - Establishing "Bifu Selection Standards": For investment tokens (RWA), Bifu deeply understands the SEC's regulatory red lines. We no longer solely pursue conceptual hype but have established screening standards centered on "Global Compliant Issuance + High-Quality Underlying Assets + Institutional-Grade Custody":

- Asset Quality: Prioritize global high-quality assets (such as high-rated bonds) where underlying assets are transparent, strictly audited, and highly liquid.

- Custody Upgrade: Prioritize projects benefiting from the repeal of SAB 121 that have integrated bank-grade custody or compliant trust structures.

- Compliance Architecture: Ensure clear project issuance structures capable of effectively isolating legal risks and maximizing the protection of investor rights.

2.Market Outlook: Global Interconnection Under New Order

With the formal enactment of FIT21, the jurisdictional boundaries between the SEC and CFTC have gradually cleared, eliminating industry panic caused by "enforcement uncertainty." This injects long-term confidence into the market, heralding the arrival of a more standardized and scalable digital asset market.

At the same time, the US is becoming the "Asset Factory" of global digital finance. Its rigorous legal framework and upgraded custody facilities guarantee asset quality but also limit direct distribution to global retail users. In the era of the great functional divergence of digital assets, the market urgently needs a hub capable of connecting "High-Quality US Assets" with "Global Retail Liquidity" to shoulder the responsibility of distribution.

VI. References

To ensure the accuracy and timeliness of information, the regulatory framework details cited in this report are based on official documents from relevant U.S. regulatory agencies. For in-depth research, it is recommended to visit the following official thematic pages:

Guiding and Establishing National Innovation for US Stablecoins Act (GENIUS Act):

https://www.congress.gov/bill/119th-congress/senate-bill/1582/text

Financial Innovation and Technology for the 21st Century Act (FIT21):

Statements related to Staff Accounting Bulletin No. 121 (SAB 121):

Disclaimer

This report is prepared by the Bifu Research Institute for informational purposes only and does not constitute investment advice, legal opinion, or endorsement of any specific asset. The digital asset market is highly volatile and risky; past performance is not indicative of future returns. Users should fully assess risks and consult professional advisors before investing.

Policy interpretations in this report are based on the regulatory environment at the time of publication. As local laws and regulations may update and adjust over time, please always refer to the latest documents published by official regulatory bodies for specific compliance requirements. Bifu assumes no legal liability for any decisions made based on this report.