Federal Reserve takes action with September rate reduction

30/10/202504:14:56

You saw the Federal Reserve cut its benchmark interest rate by 0.25% on September 17, 2025. The new target range stands at 4.00% to 4.25%. This move marks the first rate cut of the year and signals a shift in monetary policy. You can check the exact details below:

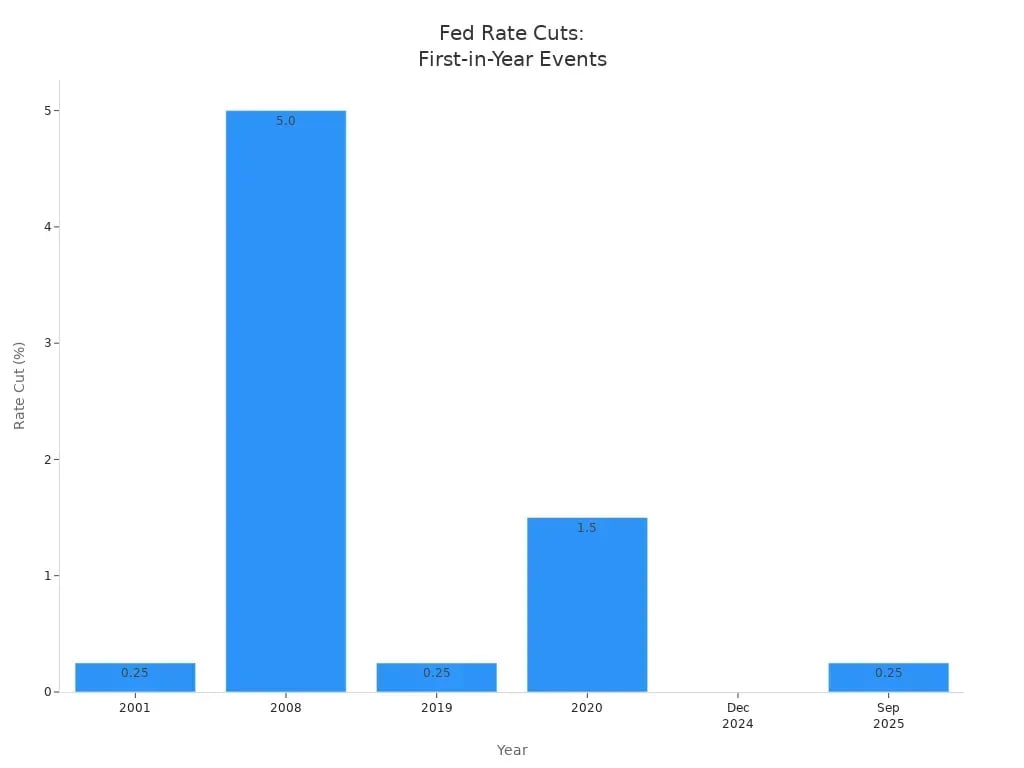

You may feel the impact if you borrow, save, or invest. The Federal Reserve rate cuts often affect loan rates, savings returns, and the stock market. This action comes as the labor market softens and inflation stays above the 2% target. The chart below shows how this rate cut compares to past first-in-year changes:

Key Takeaways

The Federal Reserve lowered its main interest rate by 0.25% on September 17, 2025. This shows the Fed now wants to help the job market more. Lower interest rates can make it cheaper to borrow money. This may help people and businesses spend and invest more. The rate cut shows the Fed is worried about fewer jobs. Unemployment is going up and there are not as many new jobs. The Fed now cares more about jobs than about inflation. Experts think the Fed might cut rates again in 2025. This could help the economy grow. Savings account interest rates may go down after a rate cut. Mortgage rates might also drop if the Fed keeps cutting rates.

Federal Reserve Rate Cuts: September 2025

Interest Rate Cut Details

The federal reserve made a new rate decision on September 17, 2025. The fed lowered its main interest rate by 0.25%. The new target range is now 4.00% to 4.25%. This is the first rate cut since December 2024. Rate cuts often mean the fed is changing its plan for money. The fed decided to cut rates because the economy is slowing down. The job market is also getting weaker.

You can look at the September 2025 rate cut and compare it to December 2024. Here is how the fed’s plan changed:

The September 2025 rate cut is about helping jobs because the job market is weaker.

The December 2024 rate cut was to control inflation and help the economy grow.

The September rate cut shows the fed cares more about jobs now than inflation. If jobs keep getting weaker, there may be more rate cuts.

Fed Decision Process

The fed uses many clues to help make rate decisions. You can read the official statement to learn why the fed cut rates. Jerome Powell, the fed chair, said:

"The labor market is really cooling off," Fed Chair Jerome Powell said at a news conference Wednesday after the announcement.

Economists also shared their thoughts about the fed’s choice:

"After weak July and August employment reports and a large negative preliminary benchmark revision, job growth now appears to be much lower and below the breakeven rate, the risks still tilt toward further negative revisions, the unemployment rate has risen slightly for two months in a row, and our broader measure of labor market slack has risen a bit more," Goldman Sachs economists wrote.

The fed looks at many reports before making a rate cut. The fed checks job numbers, unemployment rates, and other signs of how the economy is doing. The September 2025 rate cut shows the fed wants to help jobs get better. Rate cuts also make it cheaper for people and businesses to borrow money.

The fed makes rate decisions several times each year. The September 2025 rate cut means the fed is now focused on helping jobs, not just fighting inflation. The fed will keep watching the economy and may change rates again if needed. You should watch for future rate cuts and see how they change interest rates, loans, and savings.

Why the Fed Cut Rates

Economic Indicators

You may wonder why the federal reserve decided to make an interest rate cut in September 2025. The answer starts with the signals from the economy. The fed saw that economic growth was slowing down. You could see this in the numbers for GDP and consumer spending. Both showed less strength than earlier in the year. The federal reserve has a job to keep the economy healthy. It must balance two things: making sure people have jobs and keeping prices stable.

The fed noticed that prices stayed high. Inflation did not fall as much as the fed wanted. At the same time, the economy faced new challenges. Tariffs made some goods more expensive. This pushed prices up even more. You probably saw higher prices at the store. The fed had to think about these inflation risks. Still, the fed saw that the economy needed help. The slowdown in economic growth and weaker spending made the fed act.

The federal reserve must watch both jobs and prices. When the economy slows and prices stay high, the fed faces tough decisions.

You can see that the fed chose to focus on jobs this time. The interest rate cut shows the fed wants to support the economy and help people find work. The fed hopes lower rates will make it easier for you and others to borrow money, spend, and invest.

Labor Market and Inflation

The labor market gave the fed more reasons to act. You could see signs that jobs were getting harder to find. Here are some key facts about the labor market before the September 2025 rate cut:

The long-term unemployment rate rose to 1.9 million in August 2025. This was up by 385,000 from the year before. It made up 25.7% of all unemployed people, the highest since February 2022.

Initial claims for unemployment benefits jumped by 27,000 to 263,000 for the week ending September 6. This showed more layoffs.

Job growth numbers were revised down by 911,000 from April 2024 to March 2025. This means the labor market was weaker than many thought.

Confidence among people looking for work dropped to 44.9%. This was the lowest since June 2013.

You can see that the fed paid close attention to these numbers. The fed saw that more people struggled to find jobs. The fed also noticed that people felt less sure about finding new work. These signs made the fed worry about the future of the labor market.

At the same time, inflation stayed above the fed’s target. Prices for many goods and services kept rising. Tariffs made some imports cost more, which pushed prices up again. The fed had to balance these inflation risks with the need to help the labor market. You may have noticed higher prices for food, gas, and other everyday items. The fed knows that higher inflation can hurt your budget.

The fed’s decisions always try to balance jobs and prices. In September 2025, the fed saw that the risks to jobs were growing. The fed decided that helping the labor market was more important than fighting higher inflation at that moment.

You might wonder what happens next. The federal reserve expects to make more rate cuts in 2025. Here is what experts predict:

The fed may cut rates three times in 2025.

You could see at least two more cuts by June 2025.

These cuts could bring the fed’s key rate to just above 3%.

The fed will keep watching the economy, jobs, and prices. You should pay attention to how these changes affect your life. Lower rates can help you borrow money at a lower cost. They can also make it easier for businesses to grow and hire more people. The fed’s choices shape the economy, prices, and your daily life.

Market and Consumer Impact

Stock Market Reaction

The stock market changed fast after the Federal Reserve cut rates. Some big stock indices moved in different ways. The Dow Jones Industrial Average went up. The S&P 500 and Nasdaq Composite went down a little. Here is a table that shows how the main indices changed:

The Dow went up the most. Technology stocks in the Nasdaq went down. Investors moved their money to different types of stocks. Some groups, like industrials, gained value. Others, like technology, lost value. You can see these changes in the table above.

Borrowing and Mortgage Rates

You might wonder how the rate cut changes borrowing and mortgage rates. The average 30-year fixed-rate mortgage dropped to 6.35%. This is the lowest in almost a year. Experts say one rate cut does not change mortgage rates a lot right away. Mortgage rates often change before the Fed makes a move. This is because markets expect it. Mortgage rates depend on long-term trends. They do not just follow the Fed’s decision. If the Fed cuts rates again, mortgage rates may fall more later.

Here are some facts about mortgage rates after the September 2025 rate cut:

The average rate for a 30-year fixed mortgage fell to 6.35%.

Mortgage rates did not drop a lot because people expected the Fed’s move.

Experts say you should not expect a big change in mortgage rates after one rate cut.

Mortgage rates follow Treasury rates, which show long-term economic trends.

If the Fed keeps cutting rates, mortgage rates may slowly go down.

Lower mortgage rates can help you buy a home or refinance your loan.

You may see better deals on mortgages if the Fed keeps lowering rates.

Mortgage rates affect your monthly payments and the total cost of your loan.

Savings and Loans

You will see changes in savings account interest rates after a rate cut. Banks usually lower the rates they pay on savings accounts and CDs. The average yield on savings accounts was 0.52% in early September. This is just a little lower than last year. High-yield savings accounts and CDs still offer better rates, around 4% to 4.6%. Some accounts may keep rates near 4% until the end of 2025. If you have a high-yield savings account, you may notice the APY dropped from 5.55% to 4.35% after earlier cuts.

Lower rates also make loans cheaper. You may find it easier to get a personal or business loan. Banks can offer lower interest rates. This helps you borrow money for a car, home, or business. Lower auto loan rates make buying a car more affordable, even if you have a lower credit score. You may see more people spending and investing because borrowing costs are lower.

Policy and Political Context

Fed Independence

Some people talk about the federal reserve being independent. This means it makes its own decisions, not controlled by politicians. The federal reserve wants people to trust it. It stays away from political influence to keep that trust. When the September 2025 rate cut happened, officials shared their worries. They said President Trump tried to influence the federal reserve’s leadership. This could hurt its independence. The federal reserve thinks being independent helps it make good choices for everyone.

The federal reserve has problems when leaders push their ideas. Officials say independence is important for strong decisions that help the economy.

Policy Pressures

Political pressure got stronger in 2025. This pressure can change how the federal reserve decides things. Here are some examples:

Loretta Mester, who used to lead a federal reserve bank, said attacks from politicians could make people trust the federal reserve less.

David Andolfatto, an economics professor, said President Trump’s pressure on the federal reserve is stronger than ever.

President Trump said the federal reserve should have cut rates sooner.

Trump’s pick for the federal reserve board, Stephen Miran, did not agree with the rate cut and wanted a bigger cut.

Stephen Miran was the only board member who disagreed during the September 2025 rate cut.

Other board members, like Christopher Waller and Michelle Bowman, did not want to keep rates the same. This shows there was tension.

Trump tried to remove federal reserve governor Lisa Cook, saying she did something wrong. This shows politics can affect the federal reserve’s leadership.

President Trump’s actions and words add more pressure on the federal reserve’s choices.

The federal reserve has to balance being independent with these outside pressures. It tries to focus on the economy, not politics. When you watch the news, see how these pressures might change future decisions about money policy.

You notice the September 2025 rate cut makes people careful about the economy. Experts say growth is slow and inflation is close to 3%.

Keep an eye on wages, prices, and how people spend money. You might see lower interest on savings and small drops in credit card rates. Many families feel stressed because things cost more. Advisors say to think about buying good stocks, real things like property, and medium-term bonds. The Fed could lower rates again if jobs and prices stay weak. Check your money plans and look for new chances.

FAQ

What does a Federal Reserve rate cut mean for you?

You may see lower interest rates on loans and credit cards. Banks often reduce rates after the Fed acts. You could pay less for borrowing money. Savings account rates may also drop.

How soon will you notice changes in mortgage rates?

Mortgage rates may not change right away. Lenders often adjust rates before the Fed announces a cut. You should watch for slow drops over the next few months.

Will your savings account earn less interest?

Yes, banks usually lower savings rates after a Fed rate cut. You may see your account’s annual percentage yield (APY) decrease. High-yield accounts may still offer better rates than regular savings.

Should you refinance your loan after a rate cut?

You might save money by refinancing if rates drop enough. Check your current rate and compare new offers. You can ask your lender for details and see if refinancing helps you.